See for yourself. Our anemic economic performance since 2007 is . . . the best in the world?

Yes, it’s still a slow recovery that has yet to restore full employment, but, except for Germany, we’ve done better than any of our counterparts in Europe that also experienced a financial crisis.

“The ordinary will be considered extraordinary.”

I was going to say something about the folly of austerity policies (spending cuts and tax increases) during an economic slump, which is true insofar as US budget policy has been only mildly contractionary while our European counterparts have embraced austerity and all but one have sick economies to show for it, but that one is Germany, which was slightly ahead of the US as of 2013:Q2 (data for 2013:Q3 and Q4 were not available for the European countries). Germany’s economy defies easy explanation. Maybe Germany should be Luke Wilson’s character and the US can be Maya Rudolph’s.

(For anyone who’s not familiar with “Idiocracy,” here’s the trailer.)

Wednesday the Federal Open Market Committee did the expected, by announcing a “tapering” off of its $85 billion monthly purchases of long-term Treasury bonds and mortgage-backed securities (MBS’s), citing “the cumulative progress toward maximum employment.” Thursday the BLS announced that weekly jobless claims rose to their highest level in nine months. Ouch.

Granted, the spike in jobless claims might not mean much, as they can be volatile, especially around holiday time, and indeed the four-week average of jobless claims “only” rose to its highest level in one month. Even so, the “progress toward maximum employment” has been glacial, if it can be called progress at all. The media have trumpeted the good news in the Bureau of Labor Statistics’ (BLS) latest employment report, which found that the standard unemployment rate fell from 7.3% to 7.0%, its lowest level in five years, and employers added 203,000 jobs. That’s fine, but it’s also just one month. Let’s look at the past year, from Nov 2012 to Nov 2013, using the Households Survey numbers in the employment report.

In the past year the adult US population grew by almost 2.4 million. The number of people “Not in labor force” (neither employed nor actively looking for a job) also grew by slightly more than 2.4 million. The total US labor force actually fell by 25,000, and the employment-to-population ratio also fell slightly, from 58.7% to 58.6%. While it’s good news that total employment rose by 1.1 million and unemployment (and people who say they currently want a job) fell by 1.1. million, the biggest growth sector by far is “Not in labor force,” again with 2.4 million. The employment/population ratio is exactly the same now as it was four years ago, in Nov 2009. This is not progress.

I wouldn’t be an economist if I never said “On the other hand,” however, and on that hand we have the “Establishments Survey” that furnishes the other half of the BLS report. The unemployment and employment/population rates come from the Households Survey; the payroll numbers (e.g., 203,000 jobs added) come from the Establishments Survey. Average monthly payroll growth for the past year was 191,000 jobs, or more than double the puny job growth in the Households Survey (1.1 million / 12 months = 92,000 jobs per month).

What would victory look like on the jobs front? I would say 5% unemployment, which the economy had for 35 straight months in the mid-2000s, or less. (And I would want the reduction to come from job growth and not from people leaving the labor force.) How far are we from 5% unemployment? The Atlanta Fed’s handy jobs calculator has the answer. If the economy keeps on adding 191,000 jobs per month, we return to 5% unemployment in three years. If it adds just 92,000 jobs per month, we never get back to 5% unemployment, unless the labor force does a whole lot of shrinking. If we split the difference and figure the correct figure is right in the middle at 141,500, then we get there in seven and a half years, in early 2021.

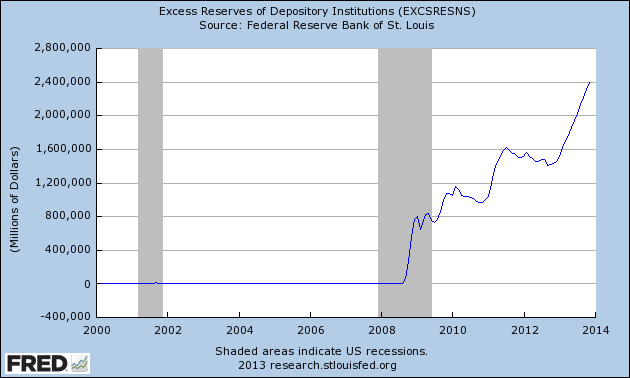

Back to the taper. The labor data suggest a need for more, not less, monetary stimulus, but how much stimulus were those emergency bond-buying programs providing? All we know is that they created $85 billion in new bank reserves each month. For the programs to work, banks needed to loan out those reserves. Not much of that has been happening:

Real estate and consumer loans are flat. Business loans are rising but not fast enough to return to their trend level. (Which, by the way, is true of just about every other macro aggregate — household consumption, business investment, etc.) Just as the fastest-growing occupational category is Not In Labor Force (NILF?), the most dramatic growth on bank balance sheets is excess reserves:

This is what pushing on a string looks like. Maybe the taper is causing the volume of loans, however meager, to be larger than it otherwise would be, but it’s hard to believe it’s making a world of difference. An oft-cited study published by the Brookings Institution found that the MBS purchases had managed to lower mortgage rates but that the Treasury bond purchases had not lowered long-term Treasury rates. And lowering long-term interest rates, as the bond buying is supposed to do, is only part of the game. Banks have to make loans at those rates. As we saw in the first graph, not nearly enough of that is happening. And the economy probably has to improve a lot more before banks are eager to lend and people are eager to borrow. Catch-22, yes.

All in all, the slight taper, from $85 billion to $75 billion a month, is unlikely to do noticeable harm, since the bond-buying program doesn’t seem to be making a big difference in the first place. Declaring victory, or even declaring substantial progress, on the employment front is foolish, but tapering is another story. Alternative policies, like ending the payment of interest (currently 0.25%) on bank reserves, might be preferable to the long-term bond-buying, but it’s clear from the last few years that Fed cannot be the main driver on the road to recovery. Congress could, through fiscal policy, but won’t, preferring austerity to stimulus, when it isn’t shutting down the government entirely. It looks like we’ll have to cross our fingers and hope for the “natural forces of recovery” to work their magic.

My views on the $85 billion meat cleaver of federal spending cuts, also known as the “sequester,” are entirely predictable to anyone who knows me or has been reading this blog. I think it’s a dumb thing to do when the economy is still weak and needs more deficit spending rather than less, it’s bad public policy to make indiscriminate cuts instead of selective cuts, and it’s not surprising that Congressional Republicans chose sequester over a balanced package of spending cuts and tax increases. I didn’t blog about it earlier because I didn’t want to be too predictable.

What’s interesting to me is that the sequester is nothing new in a sense. We had the opposite policy for two years, in the form of the 2009-2010 stimulus package, which pumped about $394 billion per year in new federal spending into the economy, and then the federal stimulus went down to about $0. The original yearly amount was about 2.5% of GDP, which should have boosted the economy quite a bit. Many leading estimates are that it did. The Commerce Department’s Bureau of Economic Analysis breaks down the contribution to GDP growth of the different components (household consumption, business investment, government purchases, net exports). Their estimates are that the federal government’s contribution to economic growth was just 0.74 percentage points in 2009 and a minuscule 0.14 points in 2010. (In both years, consumption and investment accounted for most of the change in GDP.) Possibly those numbers are underestimates and they probably do not account for any “multiplier” effects on consumption (people get money from the government and go out and spend it, etc.), but what I want to focus on is the next year, 2011, when the stimulus basically ran out.

In 2011, the combined federal, state, and local government contribution to real GDP growth was -0.67 points (which looks kind of small to me considering that stimulus spending fell by about $300 to $400 billion). It wasn’t much better — -0.34 points — in 2012. A problem with fiscal stimulus is that it’s temporary — if the patient doesn’t respond immediately, Dr. Congress decides that the medicine doesn’t work or is too expensive.

The sequestration amount for 2013 is $85 billion, or roughly 0.5% of GDP. Economists’ estimates of the size of the multiplier vary, from below 1 to about 1.4, so the likely reduction in GDP would be in the range of 0.3% to 0.7%. This would definitely hurt, but keep in mind that the government was tightening its fiscal policy in 2011 and 2012, too, with negative impacts of about the same size. To further play devil’s advocate, while the sequester is bad news and bad public policy, it’s unlikely to push the economy into recession, not if consumption and investment continue to grow as fast as they did over the past three years (with an average combined contribution to growth of about 2.5 percentage points). It’s still a lousy time to cut spending and raise taxes, but in the aggregate these cuts are mild enough that they’re merely misguided, not catastrophic.

So much for our supposed big-government Keynesian president: government jobs, the emblem of New Deal anti-depression policy, have actually gotten more and more scarce since President Obama took office. Since the recovery began in June 2009, the number of public-sector jobs has shrunk by almost 3%.

Most of that reduction has been at the state and local level, but it’s striking that the decline has been fairly continuous despite the $787 billion two-year federal stimulus package in 2009-2011. As I’ve noted before, the stimulus bill took pains to ensure that nearly all of that temporary job creation would be for private contractors. And as I’ve lamented before, it’s rather hard to have effective fiscal policies when our current politics demonizes direct government job creation (i.e., giving people government jobs) as worse than doing nothing. This is all the more remarkable considering that direct job creation was the calling card of the most popular president of the last century, Franklin D. Roosevelt, whose New Deal programs created an average of three million government jobs per year in 1933-1940. One could even argue that the political success of those programs was a big part of the reason why conservatives oppose them so fiercely, at least whenever they’re contemplated by Democrats.

What’s also striking is that this pattern is in contrast to all three of the previous recessions (1981, 1990, 2001), when public-sector employment actually grew. Notably, all three of those past recessions were under Republican presidents — maybe it’s a “Nixon goes to China” phenomenon, where only conservative-seeming Republicans can get away with increasing government employment. (Then again, it’s possible that most of the action was at the state and local level, though I’d suspect that the 1980s military buildup accounted for much of the increase under President Reagan.) Most striking of all is that the ultimate Keynesian here was Ronald Reagan, who oversaw an increase of almost 4% in government jobs in the first 30 months of recovery, the most of any of these presidents. Graph from Josh Bivens of the Economic Policy Institute (hat tip: Andrew Sullivan):

The Republican “starve the beast” strategy of running up huge deficits (preferably by cutting taxes on the wealthy and raining money on military contractors) and then using them as an excuse to cut social programs is nothing new, but this interview tidbit with iconic conservative economist Friedrich von Hayek was new to me:

‘A 1985 interview with von Hayek in the March 25, 1985 issue of Profil 13, the Austrian journal, was just as revealing. Von Hayek sat for the interview while wearing a set of cuff links Reagan had presented him as a gift. “I really believe Reagan is fundamentally a decent and honest man,” von Hayek told his interviewer. “His politics? When the government of the United States borrows a large part of the savings of the world, the consequence is that capital must become scarce and expensive in the whole world. That’s a problem.” And in reference to [David] Stockman, von Hayek said: “You see, one of Reagan’s advisers told me why the president has permitted that to happen, which makes the matter partly excusable: Reagan thinks it is impossible to persuade Congress that expenditures must be reduced unless one creates deficits so large that absolutely everyone becomes convinced that no more money can be spent.” Thus, he went on, it was up to Reagan to “persuade Congress of the necessity of spending reductions by means of an immense deficit. Unfortunately, he has not succeeded!!!”’

The snippet comes from this article about David Stockman, former Republican Congressman and Reagan Office of Management and Budget Director. Another keeper:

‘The deficits were intentional all along. They were designed to “starve the beast,” meaning intentionally cut revenue as a way of pressuring Congress to cut the New Deal programs Reagan wanted to demolish. “The plan,” Stockman told Sen. Daniel Patrick Moynihan at the time, ” was to have a strategic deficit that would give you an argument for cutting back the programs that weren’t desired. It got out of hand.”’

All of which is worth remembering the next time you’re subjected to the hand-wringing of yet another media or political figure who says the deficit is our biggest problem. (Usually these people don’t bother to mention the 25 million unemployed and underemployed, or the $1 trillion output gap.) Yes, the deficit is a problem, but don’t forget where it came from, and especially don’t trust anyone who says reversing the 2001 tax cuts or cutting military spending can’t be part of the solution.

The so-called “supercommittee” of six Democrats and six Republicans, charged last summer with drafting a deal for $1.2 trillion in spending cuts over ten years, failed to do so by today’s deadline. The so-called teeth in last summer’s agreement to form a supercommittee was that Congress would either accept their proposal or submit to $1.2 trillion in automatic, across-the-board spending cuts. Is this good news, bad news, or irrelevant?

Good, says Paul Krugman. To be precise, he said that last week. His reasoning was that cutting spending is counterproductive in a time of economic depression, as it will just exacerbate the depression, so it’s best that they didn’t make a deal to cut spending. Today, he’s a bit more nuanced, noting a Bloomberg.com story about how the supercommittee’s failure is rattling markets but highlighting this aspect of the story (Krugman’s words):

‘. . . what it actually says is that market players fear that the absence of a debt deal means no stimulus. So the actual fear is not that spending won’t be cut enough, it is that it will be cut too much — which actually makes sense, and is consistent with the action in stock and bond markets.

‘But how many readers will get that? The way it’s presented reinforces the false notion that the deficit is the problem.’

Bad, says Kevin Drum. At least if you’re someone like Kevin Drum, Paul Krugman, or me, who thinks it’s foolish to cut social spending in a depression and really isn’t all that keen on slashing the social safety net in general. Unlike Krugman, Drum thinks many if not most of the automatic spending cuts will go into effect. The deal is only good if you’re a Republican who lives to cut social programs. In other words, the Democrats got rolled again, just as in the bogus “debt ceiling authorization” debate. Drum:

‘In any case, this should basically be viewed as a total victory for Republicans. Any alternative plan would have included some tax increases, so failure to come up with an alternative means that we get a big deficit reduction that’s 100% spending cuts, just like they wanted. And the 50-50 split between domestic and defense cuts was always sort of a joke. Republicans never had any intention of allowing the Pentagon’s half of the cuts to materialize, and the domestic spending half of the cuts was about as big as they wanted them to be. Big talk aside, they know bigger cuts would run the risk of seriously pissing off voters.

‘So Republicans got domestic spending cuts that were about as big as they really wanted. They know they’ll never have to implement most of the defense cuts. And there are no tax increases.’

Irrelevant, say the bond markets. The demand for ten-year U.S. Treasury bonds was actually up slightly today, whereas really bad news about the long-term U.S. fiscal position should send demand down and interest rates up. Either the market regards $1.2 trillion over 10 years as no big deal (and it is rather small compared with a national debt of $14 trillion), or they were expecting the supercommittee to fail all along. Or both.

This just in: The Federal Reserve does not control the universe.

Stated differently: The economy is in a liquidity trap (macroeconomists). Or, monetary policy has shot its wad (Pres. Obama to economic adviser Christina Romer in their first meeting, according to Ron Suskind’s Confidence Men). Krugman has been saying this for three years now, and so have a lot of other economists. But until today, I had yet to hear it from a Fed official. Fed Chairman Ben Bernanke has called for Congress to pursue a more expansionary policy fiscal policy, thus implying but not explicitly saying that the Fed has done just about all it can. But in a speech today, Chicago Fed President and Federal Open Market Committee member Charles Evans had the guts to state the obvious:

“I largely agree with economists such as Paul Krugman, Mike Woodford and others who see the economy as being in a liquidity trap: Short-term nominal interest rates are stuck near zero, even while desired saving still exceeds desired investment. This situation is the natural result of the abundance of caution exercised by many households and businesses that still worry that they have inadequate buffers of assets to cushion against unexpected shocks. Such caution holds back spending below the levels of our productive capacity. For example, I regularly hear from business contacts that they do not want to risk hiring new workers until they actually see an uptick in demand for their products. Most businesses do not appear to be cutting back further at the moment, but they would rather sit on cash than take the risk of further expansion.”

Evans went on to suggest a number of measures the Fed should still take, like buying up more mortgage-backed securities to get the housing market going (I’m still on the fence on that one — yes, this is the economy’s weakest sector, but how do you do this without reinflating the housing bubble?), while keeping mum on the subject of whether this would do anything more than just nudge the economy forward, as opposed to bringing us anywhere near full employment. I suppose the question is moot, as long as nobody else is willing to act. Congress is not only unwilling to consider fiscal stimulus but seems to be on the verge of massive budget cuts, either by following the “super committee’s” blueprint or letting an autopilot crash the plane.

. . . is how I’d describe this month’s major developments on the fiscal and monetary policy front, namely Pres. Obama’s new jobs proposal and the Fed’s decision to reallocate its Treasury bond portfolio so as to try to push long-term interest rates down.

The Fed’s decision is simpler, so I’ll start with that one. Last Wednesday the Federal Open Market Committee kept its fed funds rate target unchanged at 0-0.25% and announced that it would sell most of its short-term T-bill portfolio and replace it with longer-term T-notes and T-bonds. This is quite a bit less than the “QE3” (quantitative easing, round 3) that many in the market were hoping for, as it does not involve a net increase in the Fed’s Treasury holdings, and the stock markets took a tumble that afternoon. The media quickly dubbed the Fed’s move “Operation Twist,” after a similar action in 1961. Nobody expects this move to have more than a marginal impact, not when mortgage and other long-term interest rates are already at historic lows, but it’s hard to argue against a positive marginal impact, purchased at so little cost. A Wall Street Journal editorial notes that the 1960s Operation Twist lowered long-term interest rates by about 0.20 percentage points, and “Some experts said that was enough to make the program effective; others deemed it a failure.” It seems to me that any reduction in unemployment from this move, however small, is welcome news at a time of 14 million unemployed.

The President’s new jobs bill is a more complicated animal. (Note that they’ve dropped the term “stimulus package,” apparently out of belated recognition that “jobs bill” is simpler and sounds more appealing and also because the $787 billion stimulus of 2009 is unpopular. I’ve been over this one before: leading estimates are that it saved a few million jobs, which is good, but it was supposed to save all of them, and that obviously didn’t happen. Thus it is unpopular.) The main complication is that it has no chance whatsoever of passing, given knee-jerk opposition to all things Obama in the Republican-controlled House and the Republican-filibuster-strength minority in the Senate. This despite the fact that, as Obama said, that virtually everything in it has been supported by Democrats and Republicans alike. (To be fair, not much in it has been supported by Republicans recently, i.e., since Obama became president.)

Specifics: The American Jobs Act (its official name) has a price tag of $447 billion, most of which apparently would be spent during the next 12 months, so roughly the same yearly amount as the 2009 stimulus. More than half of that is a $240 billion cut in payroll taxes, including a reduction in the payroll tax paid by workers, a cut in the employer share for small businesses, and a tax holiday for new employees. The next biggest item is $140 billion for infrastructure and local aid, notably transportation, retaining and rehiring teachers and first responders, and modernizing public schools. The last area is $62 billion for unemployment insurance extensions, tax credits for hiring the long-term unemployed, and subsidized employment for low-income individuals.

All of this seems reasonable, maybe too reasonable. In a less toxic political environment, this proposal would pass, but just like the 2009 stimulus, it would be way too small to fill America’s jobs deficit. The payroll tax has already been cut to 4.2% (down from about 6.2%), and the jobs bill would cut it to 3.1%, or about $11 on every $1000 of income. Small potatoes. And while poorer workers would surely spend their payroll tax cut, upper-middle class and upper-class workers would probably save much of theirs. The current payroll tax cut is set to expire at the end of this year, and Republicans aren’t crazy about it (they prefer permanent tax cuts aimed at “job creators” in the top tax brackets) but don’t want to be cast by Democrats as favoring tax increases for the little guy, so a further extension of the 4.2% payroll tax rate seems likely.

The payroll tax holiday and ($4000) tax credit for hiring the unemployed should also be expected to have a positive but marginal impact on employment. The number one question in any prospective employer’s mind is “Can I sell the extra output that this person would produce?” Tax holidays and tax credits make a Yes more likely, but only if the product demand is strong enough to almost warrant hiring the person in the first place. Still, we economists live at the margin, and as with the Fed’s Operation Twist, anything that creates jobs at minimal cost is a positive thing.

And now on to costs. This is the main area where I have a problem with the president’s proposal. Obama says the program is fully funded, when really that’s the last thing we should be worrying about during a depression.The more you offset the new spending and tax cuts with spending cuts and tax increases elsewhere, the less stimulus you have. Obama said the program will be paid for by additional spending cuts in the future, closing corporate tax loopholes, and reinstating the “millionaire’s tax” on personal income. (Note: We last had a $1 million tax bracket in 1940, in nominal terms. Adjusting for inflation, we last had a $1 million tax bracket in 1973.) If the spending cuts are sufficiently far off in the future, like when the unemployment rate is back below 6%, they should do little macroeconomic damage. Ditto the closing of tax loopholes — which probably have little to do with hiring anyway — and the millionaire’s tax. As far as I can tell, those tax increases — and some others that I would support, like taxing hedge fund managers’ salaries as ordinary labor income instead of at the lower capital gains rate — would take effect immediately. While I don’t buy the Republican rhetoric about every rich person being a Job Creator, I still don’t think raising taxes in a depression is a good idea. It can wait.

Eric Alterman hits the nail right on the head right here. Just as E. Cary Brown concluded about New Deal fiscal policy in the 1930s, the problem wasn’t that Keynesian fiscal stimulus was tried and found wanting, it’s that it wasn’t tried. Or was barely tried. In the 1930s the federal deficits were too small, were largely offset by budget cutting at the state and local level, and were reversed by a misguided attempt at budget balancing in 1936-37. Sound familiar? A key difference between then and now, however, is that Pres. Roosevelt and the Democratic Congresses of the 1930s believed in direct government job creation. The New Deal added an average of 3.5 million workers per year to the federal payroll. Pres. Obama was under great political pressure to keep that number at zero, and to hope that job creation would come from tax cuts (not promising, since much of that money gets saved or spent on imports) and government contracts (also not promising, since profit-maximizing contractors try to economize on labor costs).

Alas, this famous passage by Keynes no longer seems to be true:

‘The ideas of economists and political philosophers, both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed, the world is ruled by little else. Practical men, who believe themselves to be quite exempt from any intellectual influences, are usually the slaves of some defunct economist. Madmen in authority, who hear voices in the air, are distilling their frenzy from some academic scribbler of a few years back. I am sure that the power of vested interests is vastly exaggerated compared with the gradual encroachment of ideas.’

One could argue that Keynesian economics gave way to another academic branch of economics, like monetarism or new classical economics, but I see little in recent political or policy debates to suggest that either of those schools is being consulted. What about supply-side economics, you ask? It’s not really an academic school of economics, more a fig leaf for certain vested interests. Consider for, example former Reagan budget director David Stockman’s famous admission that the Kemp-Roth/Reagan “supply side” tax cuts were really just a Trojan Horse for cutting taxes on the rich.

Speaking of Reagan, his declaration thirty years ago that “government is the problem” seems to have become the guiding light for economic policy-making in America. Score one for “the power of vested interests.”

Bruce Bartlett offers a fine economic history lesson on the U.S. top marginal tax rate. Most people know that the top rate has changed quite a bit over time. (For those keeping score: 91% from WW2 to the early 1960s; 70% till the early 1980s; 50% for most of the Reagan administration; 28% in the late 1980s; raised to 31%, then 36%, then 39.6% in the early 1990s; lowered to 35% in 2001). Bartlett compares the top tax rate with the economic growth rates during those intervals and finds basically no correlation. That, too, is not really news (and a more careful study would take other factors into account).

What is striking, however, is how the threshold level of income for the top rate has changed over time. The original income tax, at the height of the Progressive Era during the Wilson administration, set the threshold at $500,000, which is not only higher than today’s $374,000 but was in 1913. The price level has increased more than 20 times since then; adjusting for inflation, the 1913 top tax rate kicked in at $11 million.

The famous tax cuts engineered by Harding-Coolidge-Hoover Treasury Secretary Andrew Mellon in the 1920s lowered that threshold considerably (to $100,000, or $1.2 million in today’s dollars) but in real terms left it still well above today’s. Pres. Franklin Roosevelt raised both the top tax rate and the threshold to sky-high levels (79%, and a threshold that would be $80 million in today’s dollars and may have only affected one person; some called it “the Rockefeller tax”). The threshold fell to $200,000 (equivalent to about $3 million today) during WW2 and basically stayed there till the early 1980s. The “Reagan tax cuts” of 1981 lowered the threshold to $85,600 (not quite $200,000 today). The Tax Reform Act of 1986, which Reagan signed, flattened the tax system further, with a top rate of 28% that kicked in at just $30,000 (about $50,000 today). The “Clinton tax increase” raised the threshold from $86,000 to $250,000, and inflation adjustments have raised it to $374,000 today.

Notice a partisan pattern here? It’s no secret that Republicans think the rich are overtaxed and Democrats think the rich are undertaxed, but the discussion almost always focuses on the top tax rate. What’s often missing is just where the definition of “rich” begins. In the historical record, Democrats (Wilson, Franklin Roosevelt, Clinton) have tended to set the top tax threshold high, whereas Republicans (Harding, Reagan) have tended to lower it. Much of this comes down to different notions of fairness: Democrats tend to favor a progressive income tax in which richer people pay a larger share of their income and poor people pay little or none; Republicans tend to favor a flat income tax (or no income tax), in which everyone pays the same marginal rate. Having the top rate kick in at very high levels of income tends to go hand in hand with a multiplicity of different tax rates and a highly progressive tax structure, whereas having it kick in at low levels of income means a much flatter tax.

Ever since the “Bush tax cuts” of 2001 were passed, many Democrats have talked about raising the top tax from 35% back to 39.6%, but until recently I’d heard surprisingly little talk about raising the threshold.This was surprising to me, because, as Bartlett points out, many people do not regard $250,000 or even $374,000 as particularly rich — at least not if, say, you live in New York City and have a family of four. It’s rather unclever politics to talk about raising the top rate without reassuring upper-middle class people that you’re not going to raise their taxes too. Republicans, with clever simplicity, typically truncate “tax increase on the wealthy” to “tax increase,” implying that it’s a tax increase on everybody. Lately Pres. Obama has called for raising the threshold to $1 million, so that people making $374,000-$999,999 would still pay 35 cents on their last dollar of income but people would pay 39.6 cents on every dollar of income above $1 million.

It is still debatable whether raising anyone’s taxes in a depression is ever a good idea, but ideally whatever major long-term deficit reduction plan Congress passes will go into effect only when recovery is well underway and unemployment is down to, say, 7% or less. When that happens, I agree with Bartlett that raising revenues efficiently and equitably will entail raising taxes on the top brackets (either through raising rates or, better yet, closing loopholes) and raising the top tax threshold.