See for yourself. Our anemic economic performance since 2007 is . . . the best in the world?

Yes, it’s still a slow recovery that has yet to restore full employment, but, except for Germany, we’ve done better than any of our counterparts in Europe that also experienced a financial crisis.

“The ordinary will be considered extraordinary.”

I was going to say something about the folly of austerity policies (spending cuts and tax increases) during an economic slump, which is true insofar as US budget policy has been only mildly contractionary while our European counterparts have embraced austerity and all but one have sick economies to show for it, but that one is Germany, which was slightly ahead of the US as of 2013:Q2 (data for 2013:Q3 and Q4 were not available for the European countries). Germany’s economy defies easy explanation. Maybe Germany should be Luke Wilson’s character and the US can be Maya Rudolph’s.

(For anyone who’s not familiar with “Idiocracy,” here’s the trailer.)

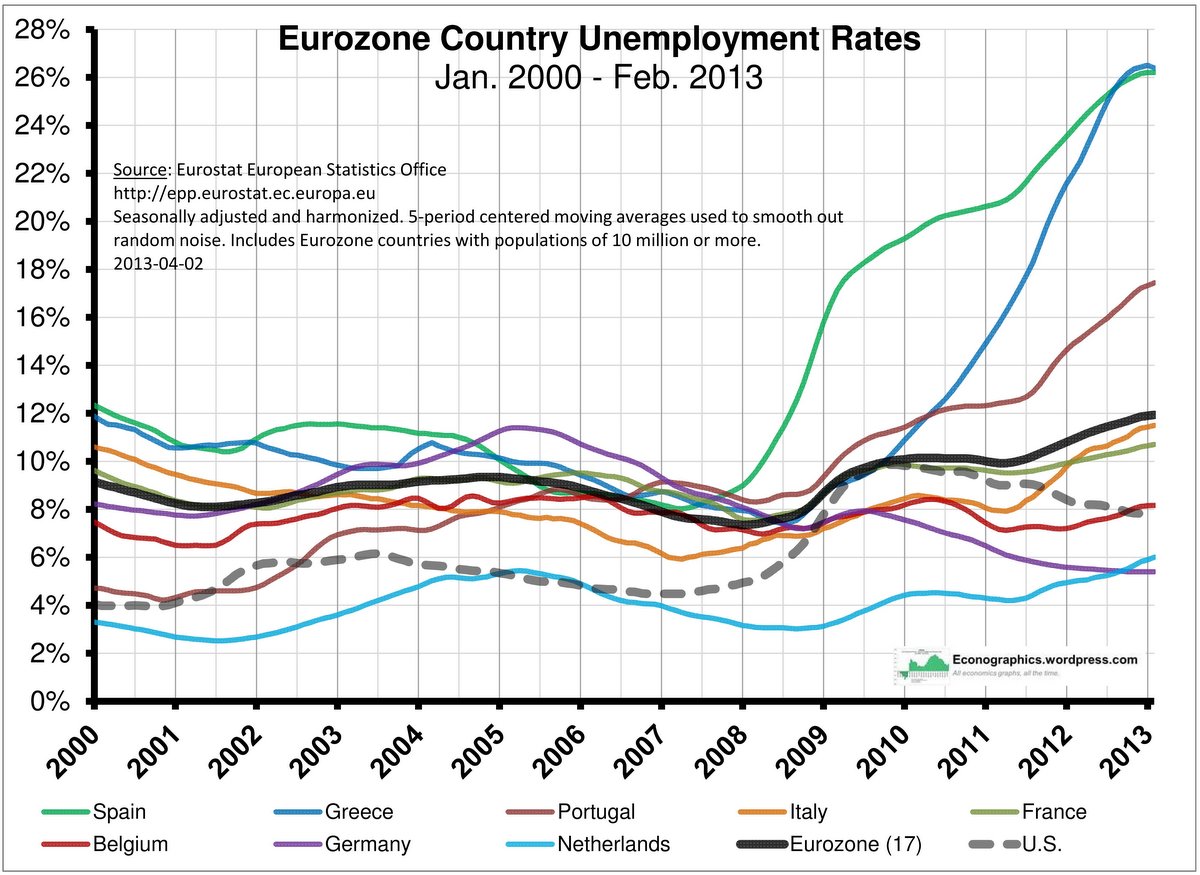

The Eurozone has had famously high unemployment rates since the euro’s inception in 1999, and for most of that time Germany has been a key sufferer, with unemployment over 8%. Since the financial crisis broke in 2008, German economic policy has been mostly associated with austerity policies, which have predictably tended to worsen Europe’s employment situation. Yet Germany’s labor market appears to have been thriving over the past five years, with an enviable unemployment rate last month of 5.4%, second-lowest in the entire 27-country Eurozone. (Relatively tiny Austria has the lowest, 4.6%.)

What accounts for the German labor market miracle? I’ve been pondering this for a while now.

First, is this miracle for real? In the US, for example, the official unemployment rate has lately been falling, yet the employment-to-population ratio has barely budged, largely because fewer people are entering the labor force (i.e., getting jobs or looking for jobs). Yet Germany’s labor force participation rate and employment-to-population ratio have been increasing. Has Germany suddenly changed its definitions of who is unemployed or not in the labor force? Apparently not, and it wouldn’t matter anyway, as these numbers are the International Labor Organization definitions of unemployment, the same as the US uses. Also, this is a fairly long-term pattern, back to 2005 (coincident with, though not necessarily caused by, Angela Merkel’s term as Chancellor following the 2005 elections).

On the other hand, perhaps Germany’s official count of the employed, like the US’s, includes a lot of part-time workers who want full-time work but cannot find it because of bad economic conditions. Indeed, The Telegraph reports:

nearly one-in-five German workers is in a tax-exempt mini-job, earning €450 a month or less. A government survey a few years ago found that nearly a third of mini-jobs workers were looking for a job with longer hours but were unable to find one.

Let’s do the math. <20% * <(1/3) = employment rate of 94.6%. Subtract 6% of 94.6%, and you’ve got 88.92%, or an unemployment rate of about 11%. This is roughly similar to the US situation, where counting involuntary part-time workers as unemployed would add 6.2 points to the unemployment rate. On the other hand, Germany’s “mini-jobs” are more a matter of government policy than their US counterparts. For more, see this Wall Street Journal article on mini-jobs, in which German experts call them dead-end jobs that provide no incentive for employers to move these workers to full-time or for the workers to give up their tax and welfare benefits for full-time work. Balance it out with this other Telegraph article that argues that mini-jobs are a helpful means of providing work.

All of this is quite different from the post I expected to write. I was going to mention how the euro’s recent weakness (for the past two years, it’s been down about 10-15% from its 2009 peak) helps Germany’s net exports. It does so both in the usual way and because Germany’s currency is surely cheaper under the euro than it would be if Germany were still on the Deutschmark. Crisis countries like Greece and Italy drag down the value of the euro, while whatever the high demand for German assets as financial safe havens does to raise the price of the euro is offset by reduced demand for other euro-country assets.

I was also going to mention Germany’s sluggish population growth and difficulty in attracting immigrants, which have caused the labor force to grow slowly. It’s easier to find jobs for a trickle of new labor force entrants than for a flood of them.

Finally, I was going to mention this 2011 National Bureau of Economic Research paper by Michael C. Burda and Jennifer Hunt, which finds the “German labor market miracle” to be real and attributes it to a hiring catch-up on the part of employers who were reluctant to hire early on in the 2000s expansion, “wage moderation” (unions accepting smaller pay increases, apparently), and “working time accounts,” seemingly similar to the “flex-time accounts” proposed by Chamber of Commerce Republicans, that allow employers to avoid paying overtime if the employee work week averages out to the standard amount. Note that the paper (or at least its abstract) does not mention “mini-jobs,” which may mean that mini-jobs are nothing new in Germany and that their use has not expanded much of late (I could not find anything much on the history of mini-jobs in my Googling).

All things considered, Germany’s labor market still looks a lot better than that of the rest of the Eurozone (except German-speaking Austria). I’d like to see a German equivalent of the comprehensive “U-6” unemployment rate that the US reports every month. My guess is that it would be very high, much like that of the US, but still showing dramatic improvement since 2005. They’re doing something right over there, but it’s hard to tell just what.

Unlike the USA and most of western Europe in 2008-2009, Canada did not have a financial crisis. Quite a few columns and articles were written about the superior stability of Canada’s financial system, which is much more concentrated but is apparently much more tightly regulated and has captured far fewer politicians and regulators than its US counterpart. I meant to blog about that but never got around to it.

Which makes Krugman’s recent post about Canada‘s still-raging housing bubble fascinating reading. In brief: housing prices in Canada experienced much the same run-up as US housing prices in the mid-2000s but instead of plummeting after 2007, have kept on rising. They are now more than double their 1975 level, whereas US house prices peaked at about 190% of that level. Canadian household debt as a percentage of income also never stopped rising and is now slightly above the US ratio.

Does this mean Canada is headed for a financial crisis? Not necessarily. Canada’s financial sector still looks sedate compared to its high-flying, reckless US counterpart. But you can have a collapsing bubble and severe recession without a financial crisis. Canada did not escape the worldwide 2008 recession and has made a fair recovery, but it is not hard to see where the next big blow could come from. Dean Baker has emphasized that the recent US financial crisis depended far less on subprime borrowing, securitization, credit default swaps, and the other usual suspects and much more on the collapse of a multi-trillion-dollar housing bubble, and the loss of all that wealth and wealth-driven consumption. Not surprisingly, Baker liked Krugman’s post. He adds that the collapse of the housing bubble could be even worse in Canada because 30-year fixed-rate mortgages never took hold in Canada (as they did in the US during the New Deal). The standard mortgage in Canada has to be paid off or refinanced in five years, so when interest rates rise from their current record lows (1% is the current benchmark short-term rate in Canada), millions of homeowners could see their monthly payments shoot up. The scenario is similar to the expiration of low “teaser rates” on adjustable-rate mortgages (ARMs) in the US in 2006-2008, but could be even worse, as the five-year limit appears more common in Canada than ARMs were in America. Could large numbers of defaults on “underwater mortgages” (where amount owed exceeds market value of house) happen in Canada, too?

I love Canada, but if I were to move there today, I’d rent.

Rising gas prices are on everyone’s mind again, as the price of oil has risen some 25% (about $25 per barrel) in the past year and the price of gasoline inches ever closer to $4 per gallon. While 1970s-style stagflation appears unlikely — the price of oil quadrupled in 1973-75, so even another 25% or 50% increase seems comparatively small, and industry has become less oil-intensive since then — the implications for the overall economy are still not good.

Alarmists often exaggerate the importance of oil prices on the economy — the bar for ridiculousness was set last week by Donald Trump, who said the 2008 financial crisis wasn’t about the banks but high gas prices — but here in today’s inbox is Nouriel Roubini, as credentialed a Cassandra as you could ever ask for, saying:

‘Today’s fragile global economy faces many risks: the risk of another flare-up of the eurozone crisis; the risk of a worse-than-expected slowdown in China; and the risk that economic recovery in the United States will fizzle (yet again). But no risk is more serious than that posed by a further spike in oil prices.‘

Roubini does not blame the 2008 crisis on oil, but he does say that the previous three world recessions were touched off by geopolitical shocks in the Middle East — the Arab oil embargo and 1973-75, the Iranian revolution and 1979-82, and Saddam Hussein’s invasion of Kuwait and 1990-91. He links the current rise in oil prices to fears that Israel will attack Iran, which may be developing nukes but definitely has lots of oil. He says oil supplies are currently plentiful and world demand remains weak, reflecting the weak economy, but that the fear factor is driving the increase. Some players along the supply chain may be hoarding oil in anticipation of higher prices caused by a disruption of Iran’s oil production. Many investors are buying futures contracts for oil at ever-higher prices, which will tend to raise the demand for oil now (since oil now and oil later are substitutes). The NYT has a fuller analysis.

Just how much of a drag on the economy would a spike in oil and gas prices be? First, just a small increase would put the price of gas over $4 a gallon, which would seem like a psychologically important “nominal anchor” (i.e., not many would notice if gas goes from $3.96 to $3.98, but if it goes from $3.98 to $4.00, alarm bells will sound). This would likely be a blow to consumer confidence, especially now that winter is ending and longer car trips are feasible. The price of gas is probably the most closely watched economic variable, more so than GDP or inflation or unemployment or even the Dow Jones average, so this negative effect could be large. Throw in the reduction in consumers’ real income and the increase in business costs, and how big a hurt does this put on real GDP? Jared Bernstein says the rules of thumb “say a $10 increase in a barrel of oil translates into about a quarter more per gallon at the pump, and, if it sticks, could shave 0.2% off of GDP growth.” Yet unlike Roubini he puts oil #2 on his list of threats to the recovery. #1 is fiscal drag, i.e., continuing government spending cuts in our already demand-starved economy. (Europe is his #3.)

The euro has always struck me as Germany’s final success at dominating Europe. What two world wars couldn’t accomplish, the Bundesbank could. By the 1990s, Germany looked like such a model of economic rectitude that eleven of its neighbors and near-neighbors (now 16, not counting principalities) were happy to formally link their currencies to Germany, their monetary policies to a European Central Bank that was a continental version of the Bundesbank, and their fiscal policies to a treaty that said deficits and debt should be under 3% and 60% of GDP (which seemed to reflect German fiscal conservatism).

Fiscal conservatism hasn’t fared well since recession began in late 2007. Even without the countercyclical tax cuts and spending increases that many governments enacted, falling GDP has caused most countries’ debt/GDP ratios to skyrocket. Even Germany’s is now over 80%. (And contrary to conventional wisdom, it’s just not true that the European economies now facing debt crises, with the exception of Greece, were running up huge deficits and debt prior to the recession; c.f. Krugman and Dean Baker.)

The news for much of this year has been of sovereign debt crises in Greece and the other “PIIGS” countries (from the “BAFFLING PIGS” mnemonic for the first 12 euro members), Portugal, Ireland, Italy, and Spain. But the most shocking economic news for me this year was the recent report that they held a German bond auction and “nobody” came. Not really nobody, but the German government was only able sell three-fifths of the “bunds” they intended to sell. To be sure, they’d have sold more if they’d been willing to accept lower bids; these bonds were supposed to pay just 2% interest, and that’s about where the yields ended up. The linked article quotes some observers who say the weak auction was due to investor concerns that Germany might be left holding the bag for PIIGS and other euro countries that can’t pay their debts. Others have said it was mostly about currency risk, i.e., the risk that the euro might massively depreciate or even crack up over the 1o-year lifetime of the bonds.

Could a euro crack-up happen? Some experts think it actually will happen, perhaps soon. Peter Boone & Simon Johnson:

‘The path of the euro zone is becoming clear. As conditions in Europe worsen, there will be fewer euro-denominated assets that investors can safely buy. Bank runs and large-scale capital flight out of Europe are likely.

‘Devaluation can help growth but the associated inflation hurts many people and the debt restructurings, if not handled properly, could be immensely disruptive. Some nations will need to leave the euro zone. There is no painless solution.

‘Ultimately, an integrated currency area may remain in Europe, albeit with fewer countries and more fiscal centralization. The Germans will force the weaker countries out of the euro area or, more likely, Germany and some others will leave the euro to form their own currency. The euro zone could be expanded again later, but only after much deeper political, economic and fiscal integration.’

At least the run on the euro is off to a slow start. The euro has had a rough November, but its decline against the dollar was only four and a half cents, or about a penny per week. The euro’s price against the dollar is still higher now than it was in most of 2005-2006.

As has been noted, euro membership has arguably gone from a privilege to a bane for these weaker countries, and possibly for all of them. Before the recession, their governments and firms could borrow cheaply on the international market, as the relatively stable euro provided insurance for the lenders, against getting repaid in devalued currency. But now euro membership takes away two key stabilization tools for them: monetary stimulus from their own central bank, and currency adjustment (a devaluation could help GDP through increased net exports).

The messy euro situation looks like the big wild card for the U.S. economy. (Here the conventional wisdom is actually correct, in my view.) Although the blow to U.S. exports from a double-dip European recession could theoretically be offset by more expansionary fiscal policy, the political prospects for additional stimulus have been dim for a long time. Things would have to get a whole lot worse here before any new stimulus could get past the Republicans in Congress, and maybe not even then.

“Italy Is Now the Biggest Story in the World,” says Kevin Drum. And he’s not talking about Joe Paterno (whose story I confess to having spent a lot more time following lately than Italy’s). But this is bad: another Eurozone country with a high debt/GDP ratio, soaring interest rates on its government debt, and no currency of its own that could depreciate to revive net exports, and no central bank of its own to expand the supply of credit. Just like Greece, except that Italy’s economy is about six times as large. It’s the fourth-largest economy in all of Europe, in fact.

For months people have been nervously watching Europe’s toxic cauldron of economic depression, austerity, sovereign debt crises, and bank funding problems (verging on crisis), and wondering if and when Europe’s problems might lead to a double-dip recession (or, as I’d call it, a recession within a depression, a la 1937). I wonder if someone else has already written the headline “Italy: Waiting for the Other Boot to Drop” yet.

P.S. If you’ve never heard the expression “Mingya!” then you obviously don’t live in Oswego. The Urban Dictionary will set you straight.

The third-quarter GDP growth numbers are better than originally reported, as today the Commerce Department revised them from their 2.0% initial estimate up to 2.5%. As many commentators have no doubt noted, that’s still short of the 3.0% thought to be necessary to reduce the unemployment rates. But we should not stop there. The more I look at the quarterly GDP figures, especially in the Commerce Department’s full report, which includes a table that breaks down the contribution to percent change in real GDP from each of the main components, i.e., consumption, business investment, government purchases, and net exports, the more it looks like a real recovery is underway.

Looking over those GDP breakdowns over time, a couple patterns emerge. First, as is often noted, fluctuations in business investment tend to be the key to recessions and recoveries. Investment is highly volatile, more so than consumption, and it tends to lead the business cycle. Second, net exports are even more volatile and, unlike investment, don’t have much of a cyclical pattern. They seem to be mildly countercyclical (in a recession that hits the whole world evenly, our imports would fall more than our exports would, simply because we our imports are much larger than our exports to begin with), but whatever cyclical pattern exists seems to be swamped by other fluctuations: just eyeballing the numbers, the GDP contribution of net exports looks like one of those “random walks.” Consider net exports’ percent contribution to real GDP over the past five quarters (i.e., since recovery officially began, or 2009:III-2010:III):

-1.37

1.90

-0.31

-3.50

-1.76

Not much of a trend there –close to -1.5% in the first quarter of the recovery, sharply positive in the second, near zero in the third, huge and negative in the fourth, back around -1.5% in the fifth. These big fluctuations can drive the quarterly real GDP changes, masking what’s happening in the domestic economy. Officially, real GDP over the past five quarters grew by the following amounts (seasonally adjusted at an annual rate:)

1.6

5.0

3.7

1.7

2.5

Again a lot of fluctuation, with the strongest readings coming the two times when net exports’ contribution was either positive or near zero. If we omit net exports to get a closer look at actual domestic spending (i.e., C+I+G, or “domestic absorption,” as development economists call it), the growth of the rest of real GDP over the same span looks like this:

3.0

3.1

4.0

5.2

4.3

A much clearer picture: GDP grew slowly in the first two quarters of the recovery, and thereafter at a much faster clip, about 4%-5%. It looks to me like the domestic U.S. economy has been recovering a respectable pace in 2010. While net exports may continue to be a drag on the economy in the future, especially as our European trading partners opt for the bloodletting approach to their economies, their extreme fluctuation makes me leery of making a definite prediction about net exports. I feel safer in saying that consumption and investment seem to be leading the U.S. recovery and that investment will hopefully pick up further as more businesses come to believe that a genuine recovery is underway.

Everyone from the Chinese to Alan Greenspan is slamming the Fed’s new round of longer-term bond purchases (QE2) as a back-door plot to weaken the dollar. The logic is that the bond purchases should lower interest rates, thereby lowering the demand for dollars and causing the dollar’s price to fall, thereby raising U.S. net exports. That much is true, but it leaves one thing out:

That’s exactly how expansionary monetary policy is supposed to work!

It’s even in a lot of macroeconomics principles textbooks: When the Fed lowers interest rates, the lower rates are supposed to raise GDP by spurring household consumption and business investment (that much is in every principles textbook) and secondarily by lowering the demand for U.S. bonds, thus lowering the demand for dollars and weakening the dollar, thus raising U.S. exports and lowering our imports. This effect is sketchier than the effects on consumption and investment, since net exports are very volatile and do not respond quickly to changes in exchange rates, but it is there.

So why exactly is it currency manipulation when it’s part of QE2 (which is only expected to reduce interest rates by about 20 basis points and so far has actually seemed to raise them a bit, due to inflationary expectations and the Fed’s surprise decision to concentrate its purchases on medium- rather than long-term bonds) but not when it’s part of the Fed’s zero-federal-funds-rate policy? I’m thinking the selective outrage might have something to do with President Obama’s meetings with Asian and G-20 leaders this week. The Chinese are happy to grasp at this new straw in order to deflect attention from their more blatant attempts to keep the yuan low, the Europeans are seeking some company for their draconian budget-slashing misery, and Greenspan is bandwagon-jumping as usual.

P.S. Although I think this particular criticism of QE2 is bogus, I am against QE2 for a host of other reasons, which I’ll get to in another post sometime.