Seriously. National Prohibition was the culmination of some eighty years of state and local prohibitions. Its “failure” discredited alcohol prohibition so badly that almost all states discarded it quickly. Countywide prohibition still exists in some of the Deep South (though not in any major cities, as far as I know), and many small townships are still dry, but drinkers today are rarely unable to obtain a legal drink, and that’s been the case for decades.

A few years before Prohibition went into effect under the Eighteenth Amendment in 1920, about 32 states had gone dry and 15 had “local option” prohibition (which was basically a way to encourage and hasten county-level prohibitions). The local option movement in particular had been very successful; about two-thirds of the states had local option by 1913. (After 1913 about half of the local option states went all in for state prohibition, likely in connection with the Anti-Saloon League’s drive for national prohibition. But even before that big drive, there were about 10 dry states and 30 local option states in 1910.) Few of the state prohibitions imposed in the forty years before Prohibition were repealed — that is, not until national Prohibition was repealed. It’s entirely possible that many of those states would have stayed dry for a long, long time, maybe even to this day, if the prohibitionists had quit while they were ahead instead of trying to impose prohibition everywhere.

Yet nearly all of those historically dry states gave up the ghost on prohibition shortly after national Repeal in 1933. Only a handful of states, if I recall correctly, kept their statewide bans through 1940. The last holdout was Mississippi in 1966. My point — and I do have one! — is that the apparent abject failure of national Prohibition probably discouraged many temperance-minded politicians and electorates from holding onto prohibition at the state or local level.

Are you saying Prohibition wasn’t an abject failure? You’re not saying it was a success, are you? No, but it was a qualified failure, not a complete failure. (This is the general consensus among historians, by the way. Jack S. Blocker, Jr.’s article “Did Prohibition Really Work?” is a good place to go for the details.) Alcohol consumption did fall during Prohibition; according to careful estimates by economists Jeffrey Miron and Jeffrey Zwiebel, who are anything but pro-Prohibition, alcohol consumption fell about 70% early on and regained only about half of that decline in later years. Prohibition seemed to work well enough in rural areas, small towns, socially conservative areas, and generally where there was widespread support for it. Which was a lot of the nation, especially acreage-wise. (This is kind of like those red-vs-blue county-level maps of support for Republicans vs. Democrats in presidential elections.) Prohibition failed in the cities, where drinking was more popular than temperance. It failed spectacularly in New York City and Chicago, the nation’s two largest cities at the time. Press coverage of speakeasies, flappers, Al Capone, and general flouting of Prohibition in the nation’s two largest media markets would tend to give a skewed impression of how Prohibition was faring nationally. “Prohibition was a failure” became such strong conventional wisdom that virtually nobody thinks of bringing it back. Even some of those few dry holdout towns, like the ones I’ve working on a paper on (Kensington, Takoma Park, and Damascus, Maryland), have jumped on the wet wagon.

We can also thank Prohibition for the death of the old all-male saloon, which gave way to the fuller inclusion of women in our drinking places and rituals. (See Catherine Gilbert Murdock’s excellent book “Domesticating Drink” for a fuller account.) Prohibition spawned countless new cocktails, as spirits, being much more easily concealed than beer, soared to new heights of popularity. While Prohibition’s unintended legacy isn’t all positive — for example, it made American beer even blander and more homogenous (I have a paper on this that I can send you) — the perception that it failed outright arguably means that the overwhelming majority of American drinkers can get a drink wherever they want. Speaking of which . . .

April 7 occupies a special place in American beer history. Despite the title of the post, it’s a good place.

On April 7, 1933, after thirteen years of Prohibition, Americans could legally drink beer again. Thus, National Beer Day. But there was a catch.

Prohibition wasn’t over. The 18th Amendment, which gave us national prohibition, would not be repealed until December 5. Although Congress had already voted for the repeal amendment on February 20, that amendment still needed the approval of three-fourths of the states to become law. That approval happened in record time, by December 5, but that’s still eight months later than April 7. So what happened on April 7?

April 7 was the date designated by Congress for legal sales of “non-intoxicating” beer and wine, in a law passed on March 22, as the states began the process of ratifying the repeal amendment. (The first state to do so was Michigan on April 10, so Michiganders get yet another day of celebration.) The law was called the Beer-Wine Revenue Act (or the Cullen-Harrison Act, for its sponsors). It basically said that alcoholic beverages that were 3.2% alcohol (by weight, that is, which equates to 4% by volume, or ABV) were not intoxicating. That mattered because the Prohibition amendment had outlawed the manufacture, distribution, and sale of intoxicating liquors, without specifying a threshold for “intoxicating.” The enforcement act for Prohibition, the Volstead Act, defined intoxicating as anything over 0.5% alcohol by weight. So the Cullen-Harrison Act simply changed the definition of “intoxicating.”

Now, generations of college students could tell you that “3.2 beer” can be plenty intoxicating, as long as you drink enough of it, but that’s beside the point. The point is that Americans were thirsty for beer, as Prohibition didn’t do much to hurt wine and spirits consumption but seems to have had a devastating impact on the beer market. “3.2 beer,” or 4% ABV beer, is some weak tea, as most mainstream beers today are 4.5-5.0% ABV and most craft beers are 6.0% or (often much) higher, but people took what they could get.

So if you want to do National Beer Day right, find yourself a beer that’s 4% ABV or less. And good luck with that — even Mich Ultra is 4.2%. I’m celebrating with a 7 oz. Miller High Life “pony” (4.5%), which is the lowest ABV I could find.

PS For full-strength beer, December 5 — Repeal Day — is your day. By the way, I’m intrigued by the claim of the F.X. Matt brewery in Utica, which makes Utica Club beer, that Utica Club was the first beer served after Prohibition, on December 5. Seems unlikely, as other breweries had been at it for eight months and probably had some full-strength beers ready to go at the stroke of midnight on December 5. But I’d love for someone at the brewery to try to convince me.

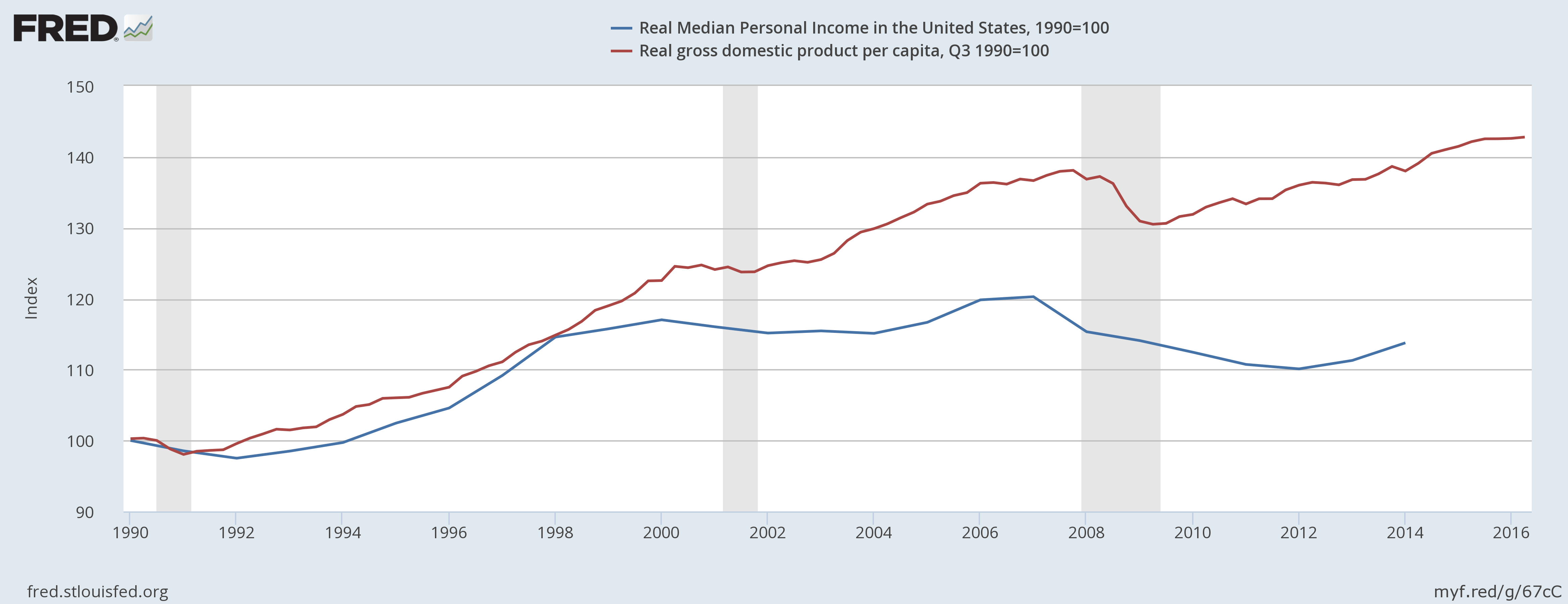

Unemployment at 4.9%. More than 75 straight months of continuous job growth. Per capita GDP at an all-time high. Summer’s here. But nobody’s dancing in the streets.

Here are a couple graphs that may help explain why:

First, note that even as real per capita GDP continues to reach new peaks, the typical American adult (i.e., the person at the 50th percentile) in 2014 was no better off than in the last two recessions. Median personal income was down about 5% from about a decade ago. The rising tide is clearly not lifting all boats. The more politicians crow about the improving economy and the more economists say we are at “full employment,” the greater the disconnect becomes.

Caveat: Ideally I’d have median personal income data from after 2014. The numbers have likely improved since then. Jared Bernstein notes that real weekly earnings have grown almost 4% since 2014. Whether personal income has had similar growth also depends on employment trends. Which brings me to:

The above is the US “prime-age” (25-54) employment/population ratio from 1990 to present. The employment/population ratio is about 2 points lower now than then, partly because the standard unemployment rate is about 1 point higher and also because more jobless people are “out of the labor force,” i.e., not actively seeking work. Would they take work if offered it? The Bureau of Labor Statistics report for June suggests many of them would — the alternative unemployment rate including jobless “discouraged workers” and “persons marginally attached to the labor force” is 6.0%. (Add in part-time workers who’d prefer to be full-time and the rate rises to 9.6%. It’s been improving for six years but is still no better than in mid 2008 when we were in a recession.)

What’s really striking to me, and what inspired the title, is the gender breakdown of those prime-age employment/population numbers. (Sorry, the separate BLS graphs for men and women are too messy to use here, but you can Google them.) For women, the employment/population ratio has regained its 1990 level of 71%; for men, the ratio is down about 5 points, to 85%. There’s a story here, probably several. The erosion of male privilege has been a big theme of this year’s political commentary. Without getting into the politics or ethics of that, let’s just note:

These graphs indicate that it by no means a new thing, at least in the labor market. The male employment/population ratio has been falling since 1969, when it was 95%. The female employment ratio has been rising steadily since at least the late 1940s, when it was less than half the current level.

During the boom decade of the 1990s, the male employment/population ratio fell by about half a point, while the female ratio rose sharply, from 71% to 74.5%.

Male employment was hit harder than female employment during the 2008-2009 recession (men’s employment fell from 89% to 81%, women’s from 74.5% to 69%).

Men’s employment has actually risen faster than women’s during the post-2009 recovery (ratio up by about 4 points vs. 2 points), but again, the male employment ratio is down about 5 points from 1990, whereas the female employment ratio is unchanged.

This new article of mine in Business History has nothing to do with the economic and financial crisis, but it’s gotten more press than any previous article I’d written, so I thought I’d post a link here.

The link will take you to the abstract and the first page only. If you would prefer to read the full, 31-page version, then here is the deluxe link. (If for some reason it does not work, you can email me — ranjit dot dighe at oswego dot edu.)

The article in brief: This article examines the historical origins of bland American beer. The US was not strongly associated with a particular beer type until German immigrants popularized lager beer. Lager, refreshing and mildly intoxicating, met the demands of America’s growing working class. Over time, American lager became lighter and blander. By the 1880s, there was a distinct “American adjunct lager” that used rice or corn to minimize the bitterness and heartiness of the malt and hops. For the next century it would get blander still and would extend its dominance of the beer market. Why? This article emphasizes America’s uncommonly strong temperance movement, which put the industry on the defensive. Another factor was the American labor market in the late 19th and early 20th centuries, with long hours (and meals often consumed at saloons between shifts), negligible union protections, and a substantial “reserve army of unemployed” from which a tipsy worker could easily be replaced. Even before Prohibition, pale pilsners were some 85-90% of the market. (And yes, Prohibition was really bad for hearty beers.) Brewers consistently pushed their product as “the beverage of moderation,” and consumers increasingly sought out light, relatively non-intoxicating beers. The recent “craft beer revolution” is explained as a backlash aided by a changing consumer culture and improved information technology. The paper’s derives its conclusions from data on beer styles, production, and content (alcohol, hops, and malt), as well as articles and editorials in trade publications.

The latest currency news is that Treasury Secretary Jack Lew is going to put a woman’s face on US currency for the first time. That is good news, of course, and way overdue. But the devil is in the details, and so far the details are not good. I say this as a believer in women’s equality and in modern economics.

First, the bill in question is the ten-dollar bill. Why the tenner? Of the four bills we use regularly — the one, five, ten, and twenty — this is the most redundant and the one we see the least of. You need those ones and fives to make change and pay for drinks, and twenties are what come out of the ATM. If you didn’t see a ten spot for a whole month, would you even notice? So it reeks a bit of tokenism to put a woman on our least important of the top four bills. The names that have been mentioned are fine — Harriet Tubman, Eleanor Roosevelt, Sojourner Truth, etc. — but Lew’s suggestion that there might be multiple ten dollar bills, with different women’s faces, seems to compound the tokenism. There’s not one woman in US history who’s important enough to warrant her own bill?

The other big problem is that the current occupant of the ten-dollar bill is the perhaps the most deserving American of a spot on our currency: Alexander Hamilton. As one of the authors of The Federalist and then as the first Treasury Secretary, Hamilton consistently advocated for the building blocks of a modern, functioning economy, as opposed to the feudal system of slave agriculture that dominated the South or the “nation of small farmers” that Thomas Jefferson idealized (despite being a rather large slaveholding farmer himself). Hamilton’s was a lonely position at a time when about 90% of the American population lived in rural areas and was engaged in farming. And Jefferson, then as now, was the more popular, inspirational, romantic figure of the two. But Hamilton eventually prevailed, as the nation industrialized and adopted a modern system of banking, including two central banks which finally eventually evolved into the Federal Reserve System in 1913. When a central bank does its job properly, recessions, deflation, and financial panics are less severe. Their track record is far from perfect, to be sure, but that’s a debate for another thread. Jefferson opposed a central bank, as did his fellow Founding Virginian and successor, James Madison, who had the bad timing to let its lease expire just before the War of 1812, when the nation could have really used a central bank. Madison relented after the war and Congress chartered a new central bank, but its lease was allowed to expire in another bit of ill timing, just before the Panic of 1837. Read the rest of this entry »

See for yourself. Our anemic economic performance since 2007 is . . . the best in the world?

Yes, it’s still a slow recovery that has yet to restore full employment, but, except for Germany, we’ve done better than any of our counterparts in Europe that also experienced a financial crisis.

“The ordinary will be considered extraordinary.”

I was going to say something about the folly of austerity policies (spending cuts and tax increases) during an economic slump, which is true insofar as US budget policy has been only mildly contractionary while our European counterparts have embraced austerity and all but one have sick economies to show for it, but that one is Germany, which was slightly ahead of the US as of 2013:Q2 (data for 2013:Q3 and Q4 were not available for the European countries). Germany’s economy defies easy explanation. Maybe Germany should be Luke Wilson’s character and the US can be Maya Rudolph’s.

(For anyone who’s not familiar with “Idiocracy,” here’s the trailer.)

The essence of the argument is that the expected benefits of legalization far exceed the expected costs, so it’s worth doing. The benefits and costs have little do with what people normally think of as economic factors, like tax revenues and law enforcement expenditures, which are actually quite small. What matters much more is the human cost of arresting, imprisoning, and/or seizing the assets of thousands of people and putting some 20 – 30 million more of them at risk of similar punishment for their recreational behavior.

Yesterday 1.3 million jobless Americans lost their unemployment benefits, thanks to Congress’s unwillingness or inability to extend long-term unemployment insurance funding. The number could rise to 4.9 million within the next year.

Extending the unemployment benefits is a no-brainer at a time when long-term unemployment rates are still higher than in any previous postwar recession, when there are three unemployed people for every job vacancy, and the money paid out in unemployment benefits quickly gets spent, thereby boosting the still-weak economy. Support for the extension is strong among the public, liberal public policy groups, and even some prominent conservatives. But Congressional Republicans continue to block it.

I’ve heard four arguments against extending unemployment benefits beyond the current 26-week threshold.

1. It encourages idleness.

Econ 101 does indeed tell us that, other things equal, anything you do to make people’s unemployment experience more pleasant, like giving them cash, reduces their incentive to take a job. Which is which unemployment benefits normally expire after 26 weeks. But these are not normal times, not with the long-term unemployment rate at 2.6%, a higher level than in any previous recession or recovery since WW2. Yet in all of those other recessions, whenever long-term unemployment got anywhere near this high, unemployment benefits were extended. If you cut off long-term unemployment benefits, some of the long-term jobless would find jobs, but the vast majority would not, unless a million or so vacancies could somehow materialize too and employers suddenly developed a preference for long-time jobless applicants. (Currently employers have a strong preference for applicants who are not unemployed, followed by those who have only been out of work for a short spell.)

A recent empirical study published by the Brookings Institution estimates that in the absence of extended unemployment benefits the unemployment rate would be about 0.1 – 0.5% lower, which we will note that is a small fraction of the current 2.6% long-term jobless rate. And the author notes that about half of that improvement would come not from the long-term unemployed rejoining the work force but from currently employed people sticking with their jobs because of the worsening of the alternative. So the estimate becomes just 0.05% – 0.25% of the long-term jobless who would rejoin the work force if benefits were cut off. Do the math, and the estimated ratio of still-unemployed people without benefits to newly re-employed is in the range of 9-to-1 to 51-to-1. Rather high pain-to-gain ratios.

2. It hurts the long-term unemployed by lengthening their term of unemployment even further, making it even harder for them to find a job.

While it’s true that employers are reluctant to hire the long-term unemployed, this argument makes the same false assumption as in (1.), namely that the jobs are out there and the long-term unemployed just aren’t looking hard enough or aren’t willing to take them. A 3-to-1 unemployed-to-vacancies ratio should give the lie to that. And the ratio of long-term unemployed to vacancies that long-term unemployed people have a realistic shot at is surely much higher.

3. It’s no longer needed, what with the economy’s recent improvement. Real GDP grew 4.1% in the last quarter, and the unemployment rate is down to 7%.

Those numbers have dominated the recent headlines, but they’re irrelevant here. Thanks to growing productivity, real GDP is now higher than it was before the recession, but with two million fewer workers. And as I seem to write in every post, the standard unemployment rate is largely irrelevant, when millions of jobless Americans have given up looking for work, millions more have left or avoided the labor force entirely, and other millions are involuntarily working part-time because they can’t find full-time work. More relevant numbers are the 13.2% comprehensive (U-6) unemployment rate; the 58.6% employment/population ratio, which has not improved since the depth of the recession; and, of course, the 2.6% rate of long-term (27+ weeks) unemployment as a percentage of the labor force. The economy’s recent good news has largely bypassed the long-term unemployed. The best that can be said about the long-term unemployment rate is that it’s been coming down, from about 4.3% four years ago, but even then it’s still as high as at any point since the 1940s.

4. It costs money.

This is the silliest objection of all, since the amount in question ($24 billion next year) is not only less than 0.7% of the budget, but a lot of the money would be returned to the federal, state, and local government in the form of tax revenues as the unemployed spend that income. Unemployed people can be counted on to spend nearly all of their benefits, especially seeing as the benefits are small compared to their previous income; the benefits level varies by state, with most states in the range of 25-45%. While unemployment benefits cost money, so do food, clothing, shelter, utilities, and all the other necessities and commitments that people have. They’re called benefits because they provide very tangible benefits to the people who receive them, far in excess of their cost to the taxpayers. (And it should be noted that the unemployed already paid into the system when they were working and will do so again if and when they return to work.)

Whatever your opinion on this issue, there should be no doubting that long-term unemployment is one of the central problems of our time. The long-term unemployed are almost 40% of the total unemployed, which is roughly twice as high as in any previous postwar recession (see graph).

While extended unemployment benefits do more good than harm, what we need even more are jobs. Government job creation is a non-starter in Congress and apparently with the public as well, so once again we are left with the Micawber-like hope that something will turn up in the private sector.

Special no-prize to the first person who can connect that last line to this video of Keith Richards:

Six years ago this month, the US economy officially peaked. We didn’t know it till a year later when NBER made the call, but the labor market has never been the same. The unemployment rate crept upward through the summer of 2008, before exploding that fall and reaching double digits the next fall (up from 4.5% in the first half of 2007), several months after the recession officially ended in June 2009. People call that devastating eighteen months the Great Recession, but I prefer to call this whole six years (and counting) the Little Depression because the economy — and the labor market in particular — remains so depressed.

Consider the change from December 2007 to now (or rather to November 2013, the most recent month we have data for):

The adult (age 16+ population) grew by 13,411,000.

Employment shrunk by 1,887,000.

Unemployment rose by 3,262,000.

“Not in labor force” (neither employed nor actively looking for a job) rose by 12,035,000.*

(*And no, most of that does not come from old people retiring. The drop in the employment/population ratio is 4.1 percentage points if you include all of the adult population, and 3.8 percentage points if you include only those in the 25-54 age range.)

Sometimes the numbers really do speak for themselves.

Wednesday the Federal Open Market Committee did the expected, by announcing a “tapering” off of its $85 billion monthly purchases of long-term Treasury bonds and mortgage-backed securities (MBS’s), citing “the cumulative progress toward maximum employment.” Thursday the BLS announced that weekly jobless claims rose to their highest level in nine months. Ouch.

Granted, the spike in jobless claims might not mean much, as they can be volatile, especially around holiday time, and indeed the four-week average of jobless claims “only” rose to its highest level in one month. Even so, the “progress toward maximum employment” has been glacial, if it can be called progress at all. The media have trumpeted the good news in the Bureau of Labor Statistics’ (BLS) latest employment report, which found that the standard unemployment rate fell from 7.3% to 7.0%, its lowest level in five years, and employers added 203,000 jobs. That’s fine, but it’s also just one month. Let’s look at the past year, from Nov 2012 to Nov 2013, using the Households Survey numbers in the employment report.

In the past year the adult US population grew by almost 2.4 million. The number of people “Not in labor force” (neither employed nor actively looking for a job) also grew by slightly more than 2.4 million. The total US labor force actually fell by 25,000, and the employment-to-population ratio also fell slightly, from 58.7% to 58.6%. While it’s good news that total employment rose by 1.1 million and unemployment (and people who say they currently want a job) fell by 1.1. million, the biggest growth sector by far is “Not in labor force,” again with 2.4 million. The employment/population ratio is exactly the same now as it was four years ago, in Nov 2009. This is not progress.

I wouldn’t be an economist if I never said “On the other hand,” however, and on that hand we have the “Establishments Survey” that furnishes the other half of the BLS report. The unemployment and employment/population rates come from the Households Survey; the payroll numbers (e.g., 203,000 jobs added) come from the Establishments Survey. Average monthly payroll growth for the past year was 191,000 jobs, or more than double the puny job growth in the Households Survey (1.1 million / 12 months = 92,000 jobs per month).

What would victory look like on the jobs front? I would say 5% unemployment, which the economy had for 35 straight months in the mid-2000s, or less. (And I would want the reduction to come from job growth and not from people leaving the labor force.) How far are we from 5% unemployment? The Atlanta Fed’s handy jobs calculator has the answer. If the economy keeps on adding 191,000 jobs per month, we return to 5% unemployment in three years. If it adds just 92,000 jobs per month, we never get back to 5% unemployment, unless the labor force does a whole lot of shrinking. If we split the difference and figure the correct figure is right in the middle at 141,500, then we get there in seven and a half years, in early 2021.

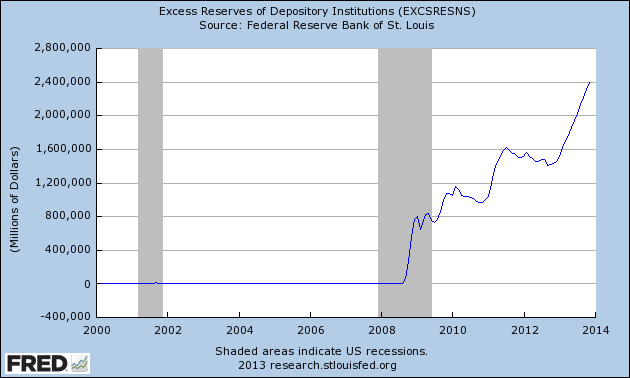

Back to the taper. The labor data suggest a need for more, not less, monetary stimulus, but how much stimulus were those emergency bond-buying programs providing? All we know is that they created $85 billion in new bank reserves each month. For the programs to work, banks needed to loan out those reserves. Not much of that has been happening:

Real estate and consumer loans are flat. Business loans are rising but not fast enough to return to their trend level. (Which, by the way, is true of just about every other macro aggregate — household consumption, business investment, etc.) Just as the fastest-growing occupational category is Not In Labor Force (NILF?), the most dramatic growth on bank balance sheets is excess reserves:

This is what pushing on a string looks like. Maybe the taper is causing the volume of loans, however meager, to be larger than it otherwise would be, but it’s hard to believe it’s making a world of difference. An oft-cited study published by the Brookings Institution found that the MBS purchases had managed to lower mortgage rates but that the Treasury bond purchases had not lowered long-term Treasury rates. And lowering long-term interest rates, as the bond buying is supposed to do, is only part of the game. Banks have to make loans at those rates. As we saw in the first graph, not nearly enough of that is happening. And the economy probably has to improve a lot more before banks are eager to lend and people are eager to borrow. Catch-22, yes.

All in all, the slight taper, from $85 billion to $75 billion a month, is unlikely to do noticeable harm, since the bond-buying program doesn’t seem to be making a big difference in the first place. Declaring victory, or even declaring substantial progress, on the employment front is foolish, but tapering is another story. Alternative policies, like ending the payment of interest (currently 0.25%) on bank reserves, might be preferable to the long-term bond-buying, but it’s clear from the last few years that Fed cannot be the main driver on the road to recovery. Congress could, through fiscal policy, but won’t, preferring austerity to stimulus, when it isn’t shutting down the government entirely. It looks like we’ll have to cross our fingers and hope for the “natural forces of recovery” to work their magic.

Heavy sarcasm aside, we do have the major stock indexes hitting record highs in a still-lousy economy. And thanks to that lousy economy and the Fed’s expansionary monetary policies in response to it, we have interest rates near record lows, which by itself does a lot to raise stock prices. (You can explain this either as borrowing costs to buy stock being cheaper than ever, as the returns on a major stock substitute [bonds] being at record lows, or as the low interest rates raising the intrinsic, or present discounted, value of future stock earnings. These explanations are not mutually exclusive.) But does that make the current stock market an out-of-control bubble? The Fed has cut interest rates many time over the decades without creating stock bubbles. Let’s take a closer look.

Since there is normally some inflation in the economy, a better way to look at stock prices is to adjust them for inflation. J.C. Parets has done this. His index was last updated for Sept 2013, at which time the real (inflation-adjusted) S&P 500 index was 1729.86 (these numbers seem to be in 2011 dollars). Parets emphasized that this amount was 20% below the real peak value of the S&P, from March 2000. But March 2000 was no ordinary peak but the height of the dot-com bubble. The market could still be grossly overvalued yet be 20% below that amount. And the market has continued to soar in the two months beyond Sept 2013; the S&P is up another 8%, so now it’s about 12% below its all-time bubblicious peak. Two lessons I draw: (1) stocks have been a lousy investment over the past 13.5 years, averaging about -1% per year in real terms, with a ton of volatility; (2) stocks could well be a bubble right now, but how large a bubble?

A still-better way to look at the stock market is the price-earnings (P/E) ratio. The measure here compares the current prices of the 500 stocks in the S&P index to their companies’ profits over the past 12 months. This chart is updated every trading day, but right now the P/E ratio is 19.87, compared with the historical averages of 14.5 (median) and 15.5 (mean). The all-time high was 123.8 in May 2009, and the all-time low was 5.3 during WWI. One could compare the current P/E of 19.87 to the historical averages and conclude that the market is about 28% overpriced (19.87 / 15.5 = 128%).

But we’re still not done. The appropriate P/E is not the same at all times. When interest rates on corporate bonds (the leading alternative to stocks) are very low and expected to stay that way for a long while, the P/E should be higher. Right now the interest rate on A-rated 20-year corporate bonds is 4.71%. An economist-approved way to compare stocks and bonds is to compare the P/E on stocks to 1/i, or 1 divided by the long-term interest rate. If investors were indifferent between bonds and stocks and cared only about their expected return, P/E and 1/i should be equal. (The 1/e ratio gives you the present-day value of a fixed-income investment that pays you $1 per year forever when the interest rate is i forever.) Right now, 1/i = 1/.0471 = 21.23, which would suggest that stocks are a bit under-priced relative to bonds. Except (if you can stand yet another about-face) there is no good reason why investors should be indifferent between bonds and stocks. Most people are risk-averse and would therefore prefer a guaranteed real return of, say 2% on bonds than an expected 2% return on stocks that could wildly fluctuate. So with normal, risk-averse investors, P/E should be somewhat less than 1/i. And with interest rates expected to rise someday, even if not any day soon, we should probably plug in a somewhat larger value of i than 4.71%. If we plug in 5% instead, then 1/i = 1/.05 = 20, just a tad higher than the current P/E of 19.87, which now looks too high. Not necessarily scary-bubble high, but overvalued just the same.

So when you think the market is a little overvalued but not necessarily a lot, should you dump your stocks? I guess that I just don’t know.

This last part is important. Larry Summers, the original front-runner for the job, helped push through the key deregulation of the late Clinton years, has dismissed the idea that it contributed to the bubble or crash, and has basically never admitted a mistake in this area. Alan Greenspan was essentially hostile to financial regulation, and bears as much responsibility as anyone for the housing bubble of the 2000s. Ben Bernanke has acknowledged that the Fed failed as a regulator during the housing bubble, but he was a Fed governor for most of that bubble and Chair for the last two years of it. Economist Bill Black finds Bernanke to have been sorely lacking as a regulator. The Fed’s main regulatory task is to try to detect and reduce systemic risk, i.e., risky activities that threaten the larger financial system and economy. Granted, Yellen told the Financial Crisis Inquiry Commission in 2010 that she failed to see several of those risks (securitization, credit rating agencies, Special Investment Vehicles) when she was San Francisco Fed President in 2004-2010, but on the other hand she was among the first at the Fed to publicly call attention to the housing bubble

Granted, monetary policy, not financial regulation, is the main part of the job. I agree with those who have said she will probably be very similar to Bernanke as far as that goes, and I’d call that a good thing. The Fed needs to do what it can to pull us out of this Little Depression, and since interest rates cannot fall below zero, additional measures like buying long-term bonds and mortgage-backed securities (i.e., quantitative easing, or QE) make sense, as long as they work. Yellen is often stereotyped as a “dove” because in recent years she favored expansionary policy and did not state that inflation was an imminent risk, but those recent years were the Little Depression that began in 2008. When unemployment is not the nation’s biggest problem, Yellen is more concerned about inflation. Such as in the roaring 1990s, when Yellen was Clinton’s Chair of the Council of Economic Advisers and then a Fed governor. With unemployment down to its lowest levels in decades, Yellen was an inflation “hawk,” as Matthew O’Brien details.

Whether the Senate is capable of that much nuance as it considers her nomination remains to be seen. I expect she’ll win majority support, including a handful of Republicans, and that Republicans will resist the temptation to filibuster her nomination. The right-leaning American Enterprise Institute offers several reasons why an anti-Yellen filibuster would be a disaster. Then again, flirting with disaster seems to be the Congressional Republicans’ game plan of late.

The Federal Open Market Committee concluded one of its most anticipated meetings in a long time with the expected decision to keep its federal funds rate target near zero (0 – 0.25%) and, less expectedly, not to “taper,” i.e., announce that it would gradually reduce its monthly purchases of mortgage-backed securities and longer-term Treasury bonds. Those purchases are otherwise known as “quantitative easing” (QE).

From various market surveys and betting sites, it appeared that about half the market was expecting a taper. Just why is hard to figure. Excessive asset purchases by the Fed can be inflationary, but excessive is in the eye of the beholder, and inflation has been under, not over, the Fed’s target of 2%. There is the argument that these new and unusual QE policies are damaging to investor confidence, but they’re not that new anymore, and the investors in the stock market seem remarkably undamaged — the S&P 500 has more than doubled since early 2009, i.e., since shortly after the first round of QE was implemented. Then there is the opposite argument that QE has created a “sugar high” in the stock market and maybe the housing market, too. This last argument has to be taken seriously, in view of how the 2000s housing bubble was stoked in part by the Fed’s easy-money policies circa 2004, when economic recovery was well underway.

But not too seriously. The S&P 500 is only about 15% higher now than it was mid-2007; adjusting for inflation, it’s hardly any higher at all (and the jury’s still out over whether stocks, as opposed to housing, were a bubble in 2007). Moreover, corporate profits are at record highs, so the fundamentals look rather good. Home prices are rising fast, but they’re still at 2004 levels, and monthly mortgage payments are cheaper than rents. A true speculative bubble is when people are obviously overpaying for assets, especially when they do so knowingly, with the plan of selling to a greater sucker later on. Is there evidence of that here?

The evidence about the general state of the economy is much stronger, and the evidence is that it’s still pretty weak. In particular, employment — the indicator that the Fed is supposed to focus on, along with inflation — is dismal. The employment-to-population ratio is still under 76%, or 4 points below where it was before the crisis. (The graph below, by the way, is of the “prime-age” population, 25-54 year-olds; if it included 16-24 year-olds, it would look even worse.)

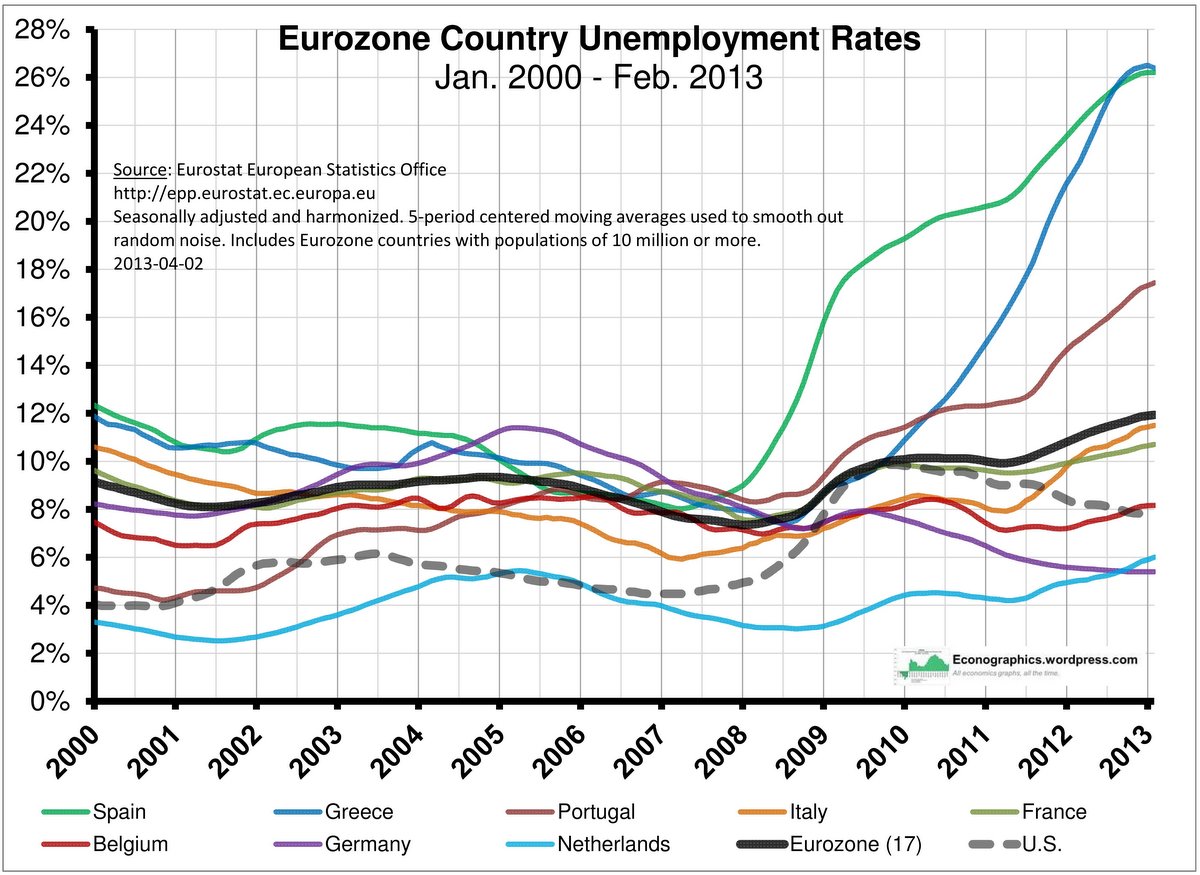

The Eurozone has had famously high unemployment rates since the euro’s inception in 1999, and for most of that time Germany has been a key sufferer, with unemployment over 8%. Since the financial crisis broke in 2008, German economic policy has been mostly associated with austerity policies, which have predictably tended to worsen Europe’s employment situation. Yet Germany’s labor market appears to have been thriving over the past five years, with an enviable unemployment rate last month of 5.4%, second-lowest in the entire 27-country Eurozone. (Relatively tiny Austria has the lowest, 4.6%.)

What accounts for the German labor market miracle? I’ve been pondering this for a while now.

First, is this miracle for real? In the US, for example, the official unemployment rate has lately been falling, yet the employment-to-population ratio has barely budged, largely because fewer people are entering the labor force (i.e., getting jobs or looking for jobs). Yet Germany’s labor force participation rate and employment-to-population ratio have been increasing. Has Germany suddenly changed its definitions of who is unemployed or not in the labor force? Apparently not, and it wouldn’t matter anyway, as these numbers are the International Labor Organization definitions of unemployment, the same as the US uses. Also, this is a fairly long-term pattern, back to 2005 (coincident with, though not necessarily caused by, Angela Merkel’s term as Chancellor following the 2005 elections).

On the other hand, perhaps Germany’s official count of the employed, like the US’s, includes a lot of part-time workers who want full-time work but cannot find it because of bad economic conditions. Indeed, The Telegraph reports:

nearly one-in-five German workers is in a tax-exempt mini-job, earning €450 a month or less. A government survey a few years ago found that nearly a third of mini-jobs workers were looking for a job with longer hours but were unable to find one.

Let’s do the math. <20% * <(1/3) = employment rate of 94.6%. Subtract 6% of 94.6%, and you’ve got 88.92%, or an unemployment rate of about 11%. This is roughly similar to the US situation, where counting involuntary part-time workers as unemployed would add 6.2 points to the unemployment rate. On the other hand, Germany’s “mini-jobs” are more a matter of government policy than their US counterparts. For more, see this Wall Street Journal article on mini-jobs, in which German experts call them dead-end jobs that provide no incentive for employers to move these workers to full-time or for the workers to give up their tax and welfare benefits for full-time work. Balance it out with this other Telegraph article that argues that mini-jobs are a helpful means of providing work.

All of this is quite different from the post I expected to write. I was going to mention how the euro’s recent weakness (for the past two years, it’s been down about 10-15% from its 2009 peak) helps Germany’s net exports. It does so both in the usual way and because Germany’s currency is surely cheaper under the euro than it would be if Germany were still on the Deutschmark. Crisis countries like Greece and Italy drag down the value of the euro, while whatever the high demand for German assets as financial safe havens does to raise the price of the euro is offset by reduced demand for other euro-country assets.

I was also going to mention Germany’s sluggish population growth and difficulty in attracting immigrants, which have caused the labor force to grow slowly. It’s easier to find jobs for a trickle of new labor force entrants than for a flood of them.

Finally, I was going to mention this 2011 National Bureau of Economic Research paper by Michael C. Burda and Jennifer Hunt, which finds the “German labor market miracle” to be real and attributes it to a hiring catch-up on the part of employers who were reluctant to hire early on in the 2000s expansion, “wage moderation” (unions accepting smaller pay increases, apparently), and “working time accounts,” seemingly similar to the “flex-time accounts” proposed by Chamber of Commerce Republicans, that allow employers to avoid paying overtime if the employee work week averages out to the standard amount. Note that the paper (or at least its abstract) does not mention “mini-jobs,” which may mean that mini-jobs are nothing new in Germany and that their use has not expanded much of late (I could not find anything much on the history of mini-jobs in my Googling).

All things considered, Germany’s labor market still looks a lot better than that of the rest of the Eurozone (except German-speaking Austria). I’d like to see a German equivalent of the comprehensive “U-6” unemployment rate that the US reports every month. My guess is that it would be very high, much like that of the US, but still showing dramatic improvement since 2005. They’re doing something right over there, but it’s hard to tell just what.

Another first Friday, another BLS employment report, and the headline news is pretty good: In July the official unemployment rate fell to its lowest level, 7.4%, since 2008. If you were a White House publicist that morning, you could have noted that fact and also that the comprehensive U-6 unemployment rate (which includes discouraged job-seekers and involuntary part-timers) also fell, from 14.3% to 14.0%. And then you could have taken the rest of the day off.

The improvement in the U-6 unemployment rate was not enough to cancel out the previous month’s 0.5% point jump. The U-6 rate was below 14% in March, April, and May. The improvement in the official (U-3) rate was exactly counterbalanced by an 0.1% point drop in the labor force participation rate (to 63.4%). The employment/population ratio was unchanged (at 58.7% for all adults, and 75.9% for prime-age (25-54) year-old adults). The decline in participation defies easy explanation, as it involves three distinct subgroups — adult white males, white teenagers, and adult black females — but not others. (A notable recent trend, by the way, is for fewer people, especially young women, to not enter the work force.)

The unemployment rates come from the BLS’s survey of households. The BLS’s other survey, of employers (the “payroll survey”), is disappointing relative to the previous month’s. June’s report showed the economy with net job growth of 195,000, plus upward revisions of 70,000 jobs to the previous two months. July’s report has net job growth of 162,000, and downward revisions of 26,000 to the previous two months. At this month’s pace, it would take us a year longer to get back to 6% unemployment than at last month’s pace (using the handy Jobs Calculator of the Atlanta Fed).

The stock and bond markets seem to have gotten this report about right. The stock market barely budged, and the 10-year Treasury bond rate actually fell somewhat, from 2.72% to 2.60%, despite the improvement in the official unemployment rate. Both markets watch the employment reports with an eye toward the Fed’s next move on interest rates and “quantitative easing” (“QE”; special purchases of long-term bonds and mortgage-backed securities), all the more so after the Fed recently announced that it would start “tapering” off QE when unemployment falls to about 7.0% and start raising its key interest rate when unemployment falls to about 6.5%. While we’re a notch closer to those rates now, the trend does not look good. Treading water is about all this labor market is doing, and the markets seem to get that.

Has the dust settled yet on last Friday’s BLS employment report? The big news was that the economy generated 195,000 new jobs in June, better than expected, and revised data show 70,000 more new jobs in April and May than previously reported. The basic unemployment rate was unchanged at 7.6%, but the new 265,000 jobs were enough to set the media and markets aflutter. Most articles I saw hailed the jobs news as fabulous. The S&P 500 had a good day, up 1.6%. Ten-year Treasury bond rates shot up 21 basis points (from 2.501% to 2.715%), in anticipation of higher interest rates to come, either from the natural forces of higher demand for credit in a stronger economy or from the Fed’s “tapering” its expansionary Little Depression-era policies.

The higher jobs numbers are welcome news, to be sure. Using the Atlanta Federal Reserve’s wonderful jobs calculator, at a rate of 195,000 new jobs per month, the US economy would be back to 6% unemployment by September 2015 and 5% unemployment by February 2017. Not great, but at least a visible end of the tunnel. For a long time the math was much more dismal — e.g., not until 2020. With the new revisions, the average job growth for 2012 is actually a bit better than June’s, 202,000. (Which, by the way, is better than in 2010 or 2011.) Plug that into the jobs calculator and we hit those targets three months sooner.

But that’s only half the story. The BLS employment report gives the results of two surveys: the “payrolls survey” of companies, above, and the “household survey” of individuals. Because these are two different survey populations, often the results are very different. The total number of jobs in the household survey rose by 189,000, but the number of new part-time jobs was more than twice that amount, 432,000. The difference is a whopping 243,000 drop in the number of full-time jobs. Ouch. The number of people working part-time because of “slack work or business conditions” rose by 352,000; the only good news here is that the number of people working part-time because they could not find full-time worked dropped a bit, by 69,000. (Hat tip: Paul Solman. The payrolls survey, by the way, does not distinguish between full- and part-time work, though it shows no change in average weekly hours, which implies no big change.)

This shift from full-time to part-time work may reflect a trend of employers’ increased preferences for part-time over full-time workers; for example, in the wholesale and retail trade sector, since 2006 full-time employment is down 500,000 while part-time jobs are up 1,000,000. Avoiding the “Obamacare” employer mandate for firms with 50+ workers would be another logical reason, and I wonder if this trend is a reason for the administration’s recently announced one-year delay of the mandate. But neither of these trends is new, so I don’t know why June would have seen such a particularly huge shift to part-time.

We see the same pattern in my favorite alternative unemployment rate, the U-6 unemployment rate, which includes part-time workers who would prefer full-time work and “discouraged workers” who want a job but have given up looking. Unlike the standard unemployment rate, which stayed at 7.6%, this comprehensive jobless shot up from 13.8% to 14.3%. Part of the rise was due to more discouraged workers, but most of it was from an increase in involuntary part-timers.

Overall, not a great employment report. It’s possible the household survey, which economists tend to regard as less reliable than the payrolls survey (even though it’s the one we use to derive the all-important unemployment rate), was just weird this month. For the past 12 months as a whole, we do not observe a shift from full-time to part-time work. The net increase in jobs was 2.4 million, and slightly under 10% of that was part-time jobs, about the same as for the labor force as a whole (i.e., including old and new jobs).

The bond market may have taken a while to digest the ambiguous nature of this report, as long-term Treasury yields, after rising sharply on the Friday of the report, lost half of that increase in the next week. The stock market continued to boom, perhaps because they see the rise in part-time employment as promising greater flexibility and profitability on the part of corporations. But of course these prices change for a lot of reasons.

Don’t worry, it’s still worth it, in a big way, at least on average. But that’s another story. This chart here has some interesting stories to tell:

(1) The big difference between average published tuition (“sticker price”) and net tuition at public four-year colleges is a big surprise to me. I teach at a four-year public college, and I don’t think we offer big tuition scholarships to all that many people. I know that some of the flagship state universities do, and those schools also have a lot more people paying high out-of-state tuition, which surely explains some of the gap. But a difference of more than a half? I would not have guessed.

— Side note: My students would no doubt point out that this chart includes only tuition and not room/board/etc., which cost a lot more than tuition at ours and many state colleges.

(2) The average net tuition paid at four-year public colleges has doubled in real (inflation-adjusted) terms in just ten years! That’s a big jump. Parents and younger siblings cannot be pleased about this.

(3) The average net tuition at private colleges is well under half the sticker price, but it’s still steep: $52,000 for four years, more if you figure that tuition inflation will continue.

(4) State schools have lost about half their relative (tuition) cost advantage to private colleges, and state school tuition is about one-fifth of private college tuition. I’m not sure which of those statistics is more significant. Overall, assuming the quality difference between public and private schools has not changed, the first point means state schools are only half as good a deal (ignoring non-tuition fee) as they used to be. But how many private colleges are five times better than public colleges (taking into account consumption value, impact on future earnings, impact on future quality of life)? Okay, throw in room, board, etc. and they are about $10.000 at both private and public, and now it’s a $12,500 net cost at public school vs. $23.000 at private school, so now the private school costs “only” 84% more. Still a big difference.

It seems the burden of proof is on private colleges to justify their huge extra cost. Depending on the college and the applicant, some are probably worth it and some aren’t. (I remember a bright student awhile back who said his father told him, “I’m not going to pay through the nose for four years just so you can screw around.”) Prospective applicants to pricey private colleges have some justifying of their own to do (hint, hint).

Lawrence Mishel’s recent piece on inequality includes a very telling graph:

We see that the second half of the 1990s is the first prolonged period when the top 1%’s income soared above that of the college educated in general; it coincided with the dot-com boom/bubble. We see a similar takeoff during the mid-2000s housing bubble and stock boom. In the market corrections/crashes that began in 2000 and 2007, we see the top 1%’s advantage mostly, but not completely, disappear.

A combination of stock options, stock-market-based bonuses, and “Takes money to make money” seems to be at work here. The graph seems to be at odds with the common argument (Greg Mankiw’s?) that the top 1% deserve all they get because they are so much more productive, as it seems doubtful that their superior productivity deserts them in bad times.

After last Wednesday, I bet Ben Bernanke can relate to this observation by George Carlin about his Catholic upbringing:

If you woke up in the morning and said, “I’m going down to 42nd street and commit a mortal sin!” Save your car fare; you did it, man!

It’s the thought that counts! The Fed didn’t “do” anything last Tuesday and Wednesday at its Federal Open Market Committee meeting. Bernanke’s concluding comments about the continuing slump were not much more specific than “This too shall pass, someday,” combined with the obvious point that normal times will bring normal monetary policies. The main news was that he thought normal times would come sooner than many people expected. But that was enough. Evidently, the bond market was expecting the economy to be flat on its back for most of the next decade: 10-year Treasury bond rates had lately been in the range of 2.1-2.2%, whereas the recent historical norm is about 5%. After Bernanke’s remarks, the rate jumped by 30 basis points (0.30% point) to a Friday close of about 2.5%. It jumped further this morning to 2.6%.

Two observations:

(1) Just as in Carlin’s church, Bernanke doesn’t actually have to do anything to tank the long-term bond market. Just thinking about it aloud is enough.

(2) The long-term bond market is really not the economy’s friend. What tanked the bond market is the prospect of interest rates rising a bit sooner and faster than expected, on account of the Fed reacting to a stronger economy. So in a weird sense the spike in bond rates is good news: Bernanke said better times were coming, the markets believed him, and they acted accordingly. Not to say that their action was malicious, just that it was predictable: if you are expecting interest rates to rise in the future, you should buy bonds in the future, not now.

My first Huffington Post column was posted last week. It’s on Ireland’s economy, against the backdrop of the G8 summit in Northern Ireland. Check it out.

The stock market would be telling the Fed something like this:

Sounds crazy, but that’s how present discounted value works. (And thanks to my daughter for the meme.)

This week the Dow fell 3% this after Fed Chair Ben Bernanke’s announcement that eventually the economy would get better and then the Fed would gradually take its foot off the accelerator. That is, the Fed would taper off its quantitative easing (QE; emergency mass purchases of long-term bonds) when unemployment (now 7.6%) fell to 7.0% and then, as announced before, would start raising short-term interest rates back toward normal levels when unemployment fell to 6.5%. He didn’t say this was going to happen soon, and reiterated that the (near-) zero interest rate policy would continue until unemployment falls to 6.5%. Granted, he sounded mildly optimistic that the economy would recovery sooner than expected, but he presented no new data on that score, so it’s an easy prediction to shrug off. Not that the markets did.

The present-discounted-value approach to stock pricing says that a stock is worth its company’s expected future profits in all years to come, divided by a discount factor that is based on the long-term interest rate. The lower the interest rate, the higher the stock’s price should be. The odd thing here is that if the economy picks up, corporate profits should too, which should offset the higher interest rates that Bernanke is hinting at. It may be that corporate profits are already high and are not always easy to predict, whereas long-term interest rates are known now. The 10-year Treasury bond rate rose from 2.2% to 2.5% after Bernanke’s announcement, a 14% increase that is right about in line with the 15% drop in stock prices. (The 10-year Treasury yield is still at a near-historic low, by the way.)

The financial media tend to report any significant-looking drop in stock prices as an economic calamity, overlooking the most basic facts about the stock market, namely that it is volatile and its short-term swings have very little macroeconomic impact. The less we worry about short-term market reaction to the Fed, the better off we’ll be. Jared Bernstein has an excellent piece on the Fed’s announcement, to which I don’t have much to add, only to say that I don’t see much new in the announcement, other than some optimistic predictions and an exit strategy for QE (which had to end sometime).

Unlike the USA and most of western Europe in 2008-2009, Canada did not have a financial crisis. Quite a few columns and articles were written about the superior stability of Canada’s financial system, which is much more concentrated but is apparently much more tightly regulated and has captured far fewer politicians and regulators than its US counterpart. I meant to blog about that but never got around to it.

Which makes Krugman’s recent post about Canada‘s still-raging housing bubble fascinating reading. In brief: housing prices in Canada experienced much the same run-up as US housing prices in the mid-2000s but instead of plummeting after 2007, have kept on rising. They are now more than double their 1975 level, whereas US house prices peaked at about 190% of that level. Canadian household debt as a percentage of income also never stopped rising and is now slightly above the US ratio.

Does this mean Canada is headed for a financial crisis? Not necessarily. Canada’s financial sector still looks sedate compared to its high-flying, reckless US counterpart. But you can have a collapsing bubble and severe recession without a financial crisis. Canada did not escape the worldwide 2008 recession and has made a fair recovery, but it is not hard to see where the next big blow could come from. Dean Baker has emphasized that the recent US financial crisis depended far less on subprime borrowing, securitization, credit default swaps, and the other usual suspects and much more on the collapse of a multi-trillion-dollar housing bubble, and the loss of all that wealth and wealth-driven consumption. Not surprisingly, Baker liked Krugman’s post. He adds that the collapse of the housing bubble could be even worse in Canada because 30-year fixed-rate mortgages never took hold in Canada (as they did in the US during the New Deal). The standard mortgage in Canada has to be paid off or refinanced in five years, so when interest rates rise from their current record lows (1% is the current benchmark short-term rate in Canada), millions of homeowners could see their monthly payments shoot up. The scenario is similar to the expiration of low “teaser rates” on adjustable-rate mortgages (ARMs) in the US in 2006-2008, but could be even worse, as the five-year limit appears more common in Canada than ARMs were in America. Could large numbers of defaults on “underwater mortgages” (where amount owed exceeds market value of house) happen in Canada, too?

I love Canada, but if I were to move there today, I’d rent.

Friday’s big economic headline was that the unemployment rate fell to 7.5%, the lowest since 2008. And payroll employment rose by 165,000, somewhat better than expected. The news was good enough to push the Dow Jones average over 15,000 for the first time, and it obviously could have been worse, but what an age of diminished expectations we are in. Almost four years since the 2007-2009 recession officially ended, and we’re at 7.5% unemployment. The comprehensive “U-6” unemployment rate, which includes all discouraged job-seekers and part-timers who want to work full time, actually edged up slightly to 13.9%. And the employment-to-population ratio was essentially unchanged at 58.5%. All not good.

As for the why and what do we do now, Jared Bernstein nails it a lot better than I could.

This weekend’s opening of the Disney blockbuster “Oz the Great and Powerful” is my opening for a little shameless self-promotion. My nearest claim to fame is a book I co-wrote called The Historian’s Wizard of Oz: Reading L. Frank Baum’s Classic as a Political and Monetary Allegory. My “co-author” is L. Frank Baum himself, as the book includes all of the first Oz book, The Wonderful Wizard of Oz, with about 65 footnotes that I put in to point out various alleged symbolism. The supposed symbols have to do with the political and economic landscape of the 1890s, when Baum wrote the book.

There are several versions of Oz as a political or monetary allegory, but almost all of them focus on farm distress (opening gloom in Kansas, a hotbed of “prairie populism”), the gold standard (yellow brick road), bimetallism (silver shoes (not ruby slippers in the book) on a yellow brick road), quest for the political power center of the nation (Emerald City), supposedly dim farmers who turn out to be quite clever (scarecrow), supposedly all-powerful president who turns out to be a “humbug” (wizard), and so on. The original allegorical interpretation, Henry Littlefield’s “The Wizard of Oz: Parable of Populism” (1964), had a symbol for seemingly every major character and incident in the book, including the name Oz as an allusion to “oz.,” the abbreviation for an ounce of gold or silver. A later version by economist Hugh Rockoff (“The Wizard of Oz as a Monetary Allegory,” 1990) added many more symbols.

The annotations in my book draw on Littlefield’s and Rockoff’s interpretations, as well as those of several others, and add a few of my own. I also have chapters on understanding the gold standard, the “Populist” farm-protest movement, and the inevitable question of whether Baum intended the book to be in any way a commentary on politics or economics. I reach a definite conclusion on that one, but I’m not going to give it away here. Besides my book, I have a freely available article in Essays in Economic & Business History that says all I have to say on the subject.

“Too big to prosecute” is the recurring headline this week after Attorney General Eric Holder’s remarkable statement before the Senate Judiciary Committee on Wednesday:

“I am concerned that the size of some of these institutions becomes so large that it does become difficult for us to prosecute them when we are hit with indications that if you do prosecute, if you do bring a criminal charge, it will have a negative impact on the national economy, perhaps even the world economy.”

Where to begin? “Too big to fail” is one thing, but to say these institutions are too big to clean up their act is another. The attorney general seems to be implying that the big banks are more important than the laws themselves. It is one thing to say that the outright collapse of these institutions would bring economic ruin. It is quite another to assume that prosecuting criminal acts by them or some of their employees would also bring ruin.

Skeptics have long called the big banks “too big to prosecute” because their lavish campaign contributions give them unparalleled access and influence in Washington, but Holder’s remarks point to something more insidious: ideological capture. When cabinet officials are products of Wall Street or, worse, credulously believe Wall Street claims that their firms are delicate life-giving flowers that must never be disturbed, we have a problem that won’t go away anytime soon.

Fortunately, several members of Congress, including Republicans David Vitter and Charles Grassley and Democrats Sherrod Brown and Elizabeth Warren, are pushing back. Vitter and Brown have co-sponsored a bill to limit the size of the big banks. But we have been here before, as recently as 2010, when a similar bill lost by a vote of 61-33 and was opposed by the Obama administration. Until further notice, it’s hard to disagree with these words of Huey Long from 1932:

“They’ve got a set of Republican waiters on one side and a set of Democratic waiters on the other side, but no matter which set of waiters brings you the dish, the legislative grub is all prepared in the same Wall Street kitchen.”

My views on the $85 billion meat cleaver of federal spending cuts, also known as the “sequester,” are entirely predictable to anyone who knows me or has been reading this blog. I think it’s a dumb thing to do when the economy is still weak and needs more deficit spending rather than less, it’s bad public policy to make indiscriminate cuts instead of selective cuts, and it’s not surprising that Congressional Republicans chose sequester over a balanced package of spending cuts and tax increases. I didn’t blog about it earlier because I didn’t want to be too predictable.

What’s interesting to me is that the sequester is nothing new in a sense. We had the opposite policy for two years, in the form of the 2009-2010 stimulus package, which pumped about $394 billion per year in new federal spending into the economy, and then the federal stimulus went down to about $0. The original yearly amount was about 2.5% of GDP, which should have boosted the economy quite a bit. Many leading estimates are that it did. The Commerce Department’s Bureau of Economic Analysis breaks down the contribution to GDP growth of the different components (household consumption, business investment, government purchases, net exports). Their estimates are that the federal government’s contribution to economic growth was just 0.74 percentage points in 2009 and a minuscule 0.14 points in 2010. (In both years, consumption and investment accounted for most of the change in GDP.) Possibly those numbers are underestimates and they probably do not account for any “multiplier” effects on consumption (people get money from the government and go out and spend it, etc.), but what I want to focus on is the next year, 2011, when the stimulus basically ran out.

In 2011, the combined federal, state, and local government contribution to real GDP growth was -0.67 points (which looks kind of small to me considering that stimulus spending fell by about $300 to $400 billion). It wasn’t much better — -0.34 points — in 2012. A problem with fiscal stimulus is that it’s temporary — if the patient doesn’t respond immediately, Dr. Congress decides that the medicine doesn’t work or is too expensive.

The sequestration amount for 2013 is $85 billion, or roughly 0.5% of GDP. Economists’ estimates of the size of the multiplier vary, from below 1 to about 1.4, so the likely reduction in GDP would be in the range of 0.3% to 0.7%. This would definitely hurt, but keep in mind that the government was tightening its fiscal policy in 2011 and 2012, too, with negative impacts of about the same size. To further play devil’s advocate, while the sequester is bad news and bad public policy, it’s unlikely to push the economy into recession, not if consumption and investment continue to grow as fast as they did over the past three years (with an average combined contribution to growth of about 2.5 percentage points). It’s still a lousy time to cut spending and raise taxes, but in the aggregate these cuts are mild enough that they’re merely misguided, not catastrophic.

President Obama proposed raising the minimum wage in his State of the Union address. Specifically he called for it to go up to $9 an hour by the end of 2015, up from $7.25 now, and then to index it to the rate of inflation in subsequent years. Is this a good idea?

Economists are famous for being against the minimum wage, with introductory microeconomics textbooks typically using it as an example of a price floor that creates a surplus of the good in question – in this case, a surplus of labor, or unemployment. And that is valid if the market for labor is perfectly competitive and if the rest of the economy is held constant. (Two rather big ifs, yes.) Economists call this “partial equilibrium analysis,” as opposed to “general equilibrium analysis,” which looks at the repercussions in all markets. In the economy as a whole, firms can’t always sell all they want to at the going price, and too-high wages are not the only source of unemployment – recessions cause unemployment, and so does falling demand in specific sectors of the economy. It’s also possible that higher minimum wages could increase the total income of the lowest-paid workers, resulting in more demand for goods and services in general and a higher level of employment. The White House clearly believes that last part (more about that here).

Who’s right? It all depends on which effect is stronger – the micro effect (higher wages mean less output and employment) or the macro effect (higher wages mean higher incomes and higher aggregate demand). And that is an empirical question. For decades, most economic studies found that minimum wages reduced employment among the least educated, least skilled workers, i.e., the people most likely to be working at low wages. But an influential study by economists David Card & Alan Krueger in the 1990s found either no effect or, surprisingly, a positive effect of higher minimum wages on low-skill or teenage employment. In their 1995 book, Card & Krueger further found that the earlier studies omitted important variables, like teenage high school attendance rates, and that controlling for those variables caused the minimum wage’s estimated effect to be insignificant. Their work has had its own critics and would-be debunkers, but it remains influential.

George F. Will once wrote, “All economic news is bad news. All economic news is good news.” Today’s GDP report has lots of both and has already sown a lot of confusion. Real GDP fell in the last three months of 2012, indicating a recession (although the drop was only 0.1%). Part of the decline came from reduced inventory investment, i.e., from companies not producing as many goods that haven’t been sold yet. So far, so bad.

The biggest decline came in government spending; in particular, military spending dropped a whopping 22%. Why? The Washington Post’s Brad Plumer says it has something to do with the drawdowns in Iraq and Afghanistan and apparently also with the various budget games that the Pentagon and other government agencies play, as regards the timing of the fiscal year and the “sequester” budget cuts that could come if Congress fails to raise the debt ceiling. One thing I learned from Plumer’s piece is that, although the 22% drop is unusually large, it’s not unusual for defense spending to drop in a particular quarter. It did so in about half of the twelve quarters from 2010 on; the second-largest drop was almost 15%.

Many people would view the big reduction in military spending as a good thing — the wars are unpopular, and some studies have found that, dollar for dollar, domestic government spending tends to create more jobs than does military spending. Aside from military spending, real GDP rose in the last quarter of 2012, by 1.3%.

Is 1.3% good? Of course not. It makes 2012:IV one of the weaker quarters of the past two years, in which the economy’s average annual growth was 2.0%. The economy grew at 3.1% in the third quarter of 2012, so this is a step backward at least in a relative sense.

But positives are not hard to find in the GDP report. Thus Bloomberg’s headline “Growth Stall Obscures Consumer, Business Pickup.” Consumer spending grew at a decent 2.2% clip, up from 1.6% in the third quarter. Rising auto sales were a big part of the increase (which sounds about right to someone like me who bought a car for the first time since 1999). I would guess that some of the slippage in inventory production was simply due to consumers buying more goods than anticipated, with the result that inventories were down. (If inventory production had not fallen, then GDP would have grown by 2.6%, according to the Bloomberg article.) The best news of all was probably on the housing front, where residential construction (counted in the “Investment” part of GDP) grew by 15%. For 2012 as a whole, housing construction rose 12%, its biggest increase since 1992.

The markets seem to have to shrugged off the report. Market participants may doubt that the increased consumer spending and construction are sustainable. Right now, five hours after the release, the Dow, S&P 500, and Nasdaq averages are basically unchanged (within 0.05% of yesterday’s close).

Remember these words: “means of extinguishment.” The full quote is “The creation of debt should always be accompanied with the means of extinguishment,” and it’s from Alexander Hamilton, the father of our national debt. Hamilton believed that the federal government could do the nation a big favor by carrying a debt as long as it had sufficient revenue streams to eventually pay it off; such an arrangement, he said, would give the US “immortal credit,” which could come in very handy whenever we had pressing needs or good public investment opportunities that justified borrowing more money.

This has been on my mind because the (yawn) “fiscal cliff” negotiations, whatever their outcome, are really just the latest round in an endless series of self-destructive battles over whether to honor our own budget commitments by raising the debt ceiling so that we can pay for them. I’ve written about Congress’s debt-ceiling looniness before, and how it would be better not to have such votes at all. Think the proposed budget has too big a deficit? Fine, then don’t vote for it. But to vote for it and then refuse to pay for it is not only cynical and hypocritical, but sows suspicion that the government is a deadbeat.

Standard & Poor’s (S&P) famously downgraded the federal government’s debt in August 2011 (from AAA to AA+), and the other two major bond rating agencies (Moody’s, Fitch) are threatening to do the same if Congress can’t reach some kind of agreement to reduce the debt/GDP ratio in the long term. After the subprime scandal, in which the rating agencies routinely rubber-stamped dodgy subprime mortgage-backed securities as AAA, these agencies have zero credibility, but that doesn’t mean they’re always wrong. The S&P said its downgrade “was pretty much motivated by all of the debate about the raising of the debt ceiling. . . . It involved a level of brinksmanship greater than what we had expected earlier in the year.” Yes — if Congress can’t be counted upon to honor its own commitments, which include paying back the principal and interest on previously issued Treasury bonds, then why should bond buyers regard Treasury bonds as completely safe? The more Congress continues to play these games, the more rational it is to conclude that maybe Treasury bonds are not so safe. Read the rest of this entry »

Today’s news from the Fed is that they will continue their zero interest rate policy (ZIRP) until the unemployment rate falls to 6.5%. To be precise, the Federal Open Market Committee (FOMC) announced that they believe the current 0 – 0.25% range for the federal funds rate “will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored.”

This replaces the Fed’s statement from six weeks ago, which was that they expected to continue the ZIRP “for a considerable time after the economic recovery strengthens” and said they thought the ZIRP would continue at least through mid-2015.

I think the new policy is better, first of all because it’s specific. Of course they’re going to raise rates when the economy’s better, but how do they define better? They just told us — 6.5% unemployment (it’s now 7.7%).

The new statement also is better because it’s a fairly clear policy rule, tied to an actual, observable number, as opposed to a prediction about when the ZIRP medicine will no longer be needed. Including a date like mid-2015 is problematic partly because predictions have a way of being wrong, but also because they have a way of creating bubbles. “Through mid-2015” was widely reported not as a prediction but as a fixed commitment by the Fed, which it wasn’t. If enough people in the financial community believe the Fed will keep rates low through mid-2015, there could be a problem. Because if they know that short-term interest rates will be low for the next three years, then they may be more likely to borrow massively in the short-term money market and invest it in longer-term risky assets while rolling over their short-term debts for the next three years. (Some people say we’re already in a stock-market bubble right now, thanks to today’s low interest rates.) Granted, “borrowing short and lending long” is what banks do, but usually it’s without the certainty of near-zero interest rates for the next three years. Read the rest of this entry »

The US unemployment rate fell to a four-year low of 7.7% in November, it was reported yesterday. The BLS (Bureau of Labor Statistics) report also noted that the economy added 146,000* jobs in November, a better figure than expected, considering Hurricane Sandy. Yet the report did not get a particularly warm reception. Analysts and cynics instantly threw cold water on these seemingly good numbers by stating that the unemployment rate fell only (or largely) because masses of unemployed people stopped looking for work in November and therefore were no longer counted as unemployed. Were they right? Off to the report’s detailed tables!